If you contribute more than your Annual Allowance to your pension pots in a single tax year, you will need to pay tax on the additional amount. If you are in more than one pension scheme, you may need to ask each pension provider to a statement in order to calculate your Annual Allowance charge.

Many of our clients take financial advice when they’re ready to withdraw their pension funds – but our advice could help avoid tax pitfalls when saving.

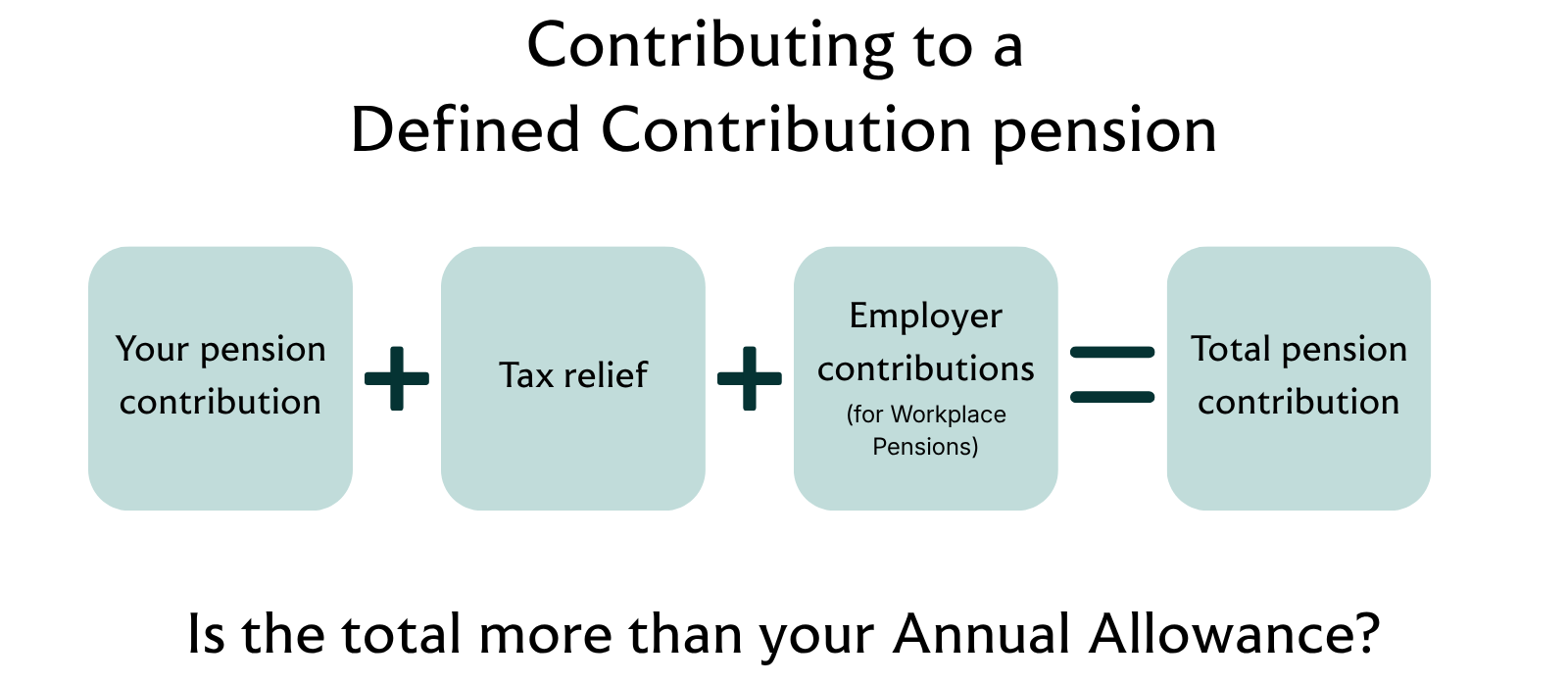

Important: This article relates to Defined Contribution (DC) pensions. If you have a Defined Benefit (DB) pension, the rules are more complex. We strongly recommend that you seek financial advice before making any decisions, as the way allowances are applied can differ significantly.

Changes to pension Annual Allowance and IHT rules may mean that some people will change how they save for the future – for example, clients faced with a tax charge may reduce or pause pension saving. We feel it’s worth reviewing the rules around pension allowances to save tax-efficiently.