Last week was dominated by Middle East conflict and rising energy prices leading to declines in both equity and bond indices. Our thoughts go out to all with friends and family affected by last week’s events and we are saddened by the human impact for those living in affected areas.

Last week

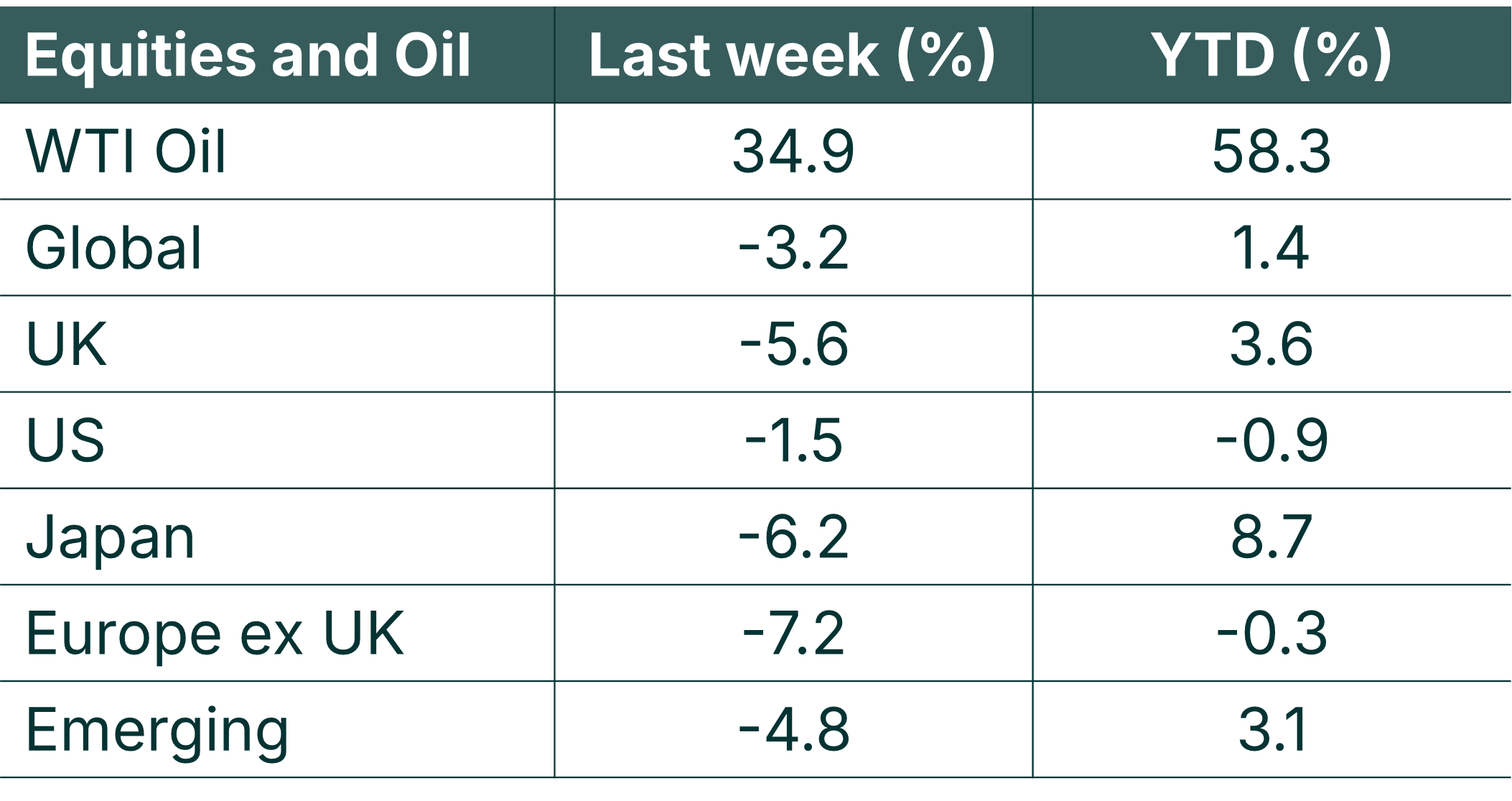

- Escalating military action between the US, Israel, and Iran sharply increased geopolitical risk, pushed WTI oil prices up by nearly 35% and drove volatility across global financial markets.

- Most tankers were unable to pass the Strait of Hormuz and the potential disruption to oil and LNG supplies together with the inflationary impact of higher energy prices weighted on global equity markets; especially for net oil importers.

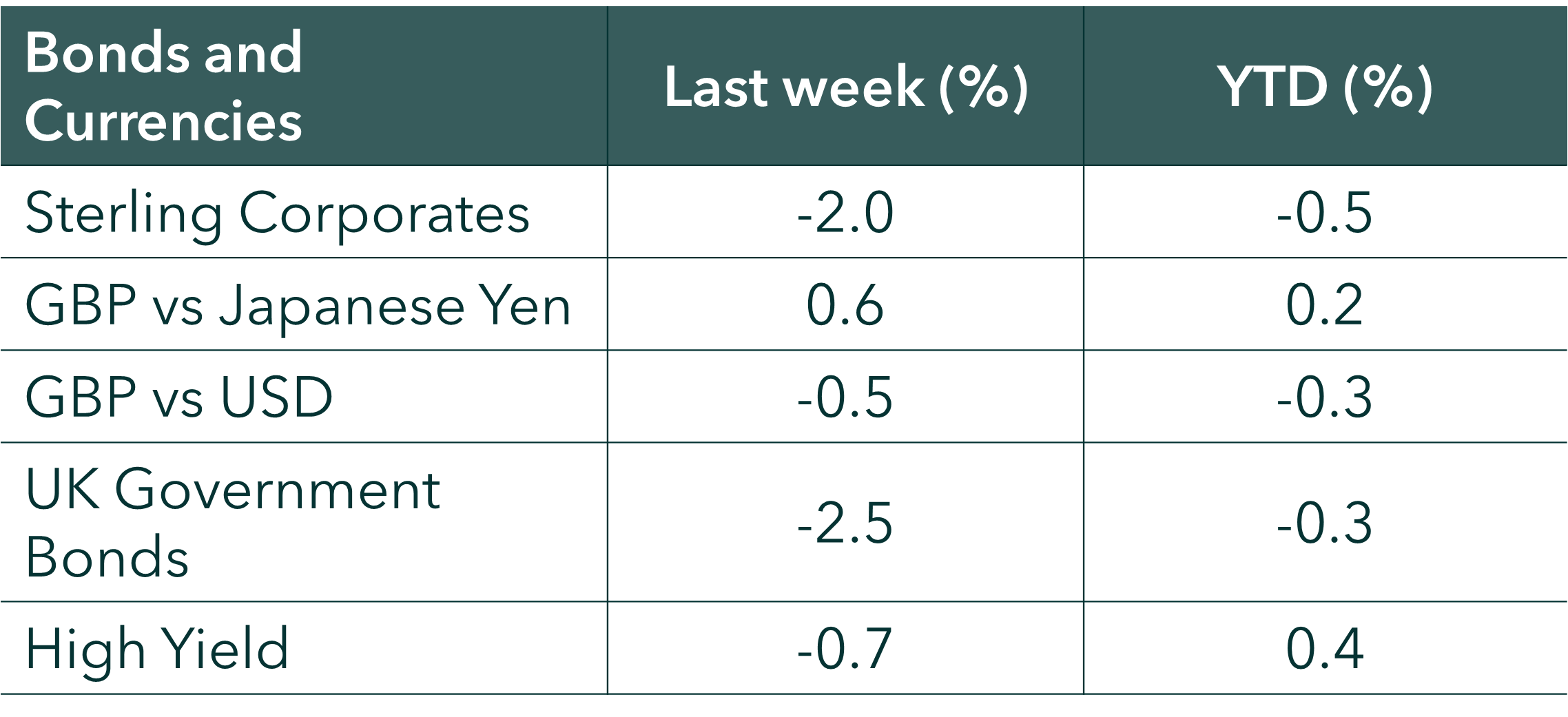

- Treasury yields rose (meaning prices fell) as higher energy prices raised inflation concerns and complicated the outlook for US interest rates. This fed through into other fixed income markets.

- On Friday the US stock market was also impacted by mixed Labour market data; ADP payrolls improved and layoffs fell, but nonfarm payrolls unexpectedly dropped by 92k, pushing unemployment to 4.4%.

This week

- US CPI inflation data for February is due on Wednesday, but market attention has shifted toward energy markets. With rising concern over supply risks and the inflationary impact of higher energy prices, the US crude oil inventory, import, and gasoline production/inventory data released the same day are likely to receive heightened scrutiny, particularly through the lens of the Middle East conflict and the potential for supply disruptions.

- US unemployment data is due on Thursday.

- Bank of England (BOE) Governor Andrew Bailey will speak on Thursday and is likely to reference the short term interest rate and inflation outlook.

- On Friday, UK GDP, production and trade balance data will be released.

Source: Bloomberg. Currency GBP.

More detail on Last Week:

- US equities came under pressure last week as markets were hit by both rising inflation concerns, driven by a sharp jump in oil prices following Middle East conflict, and renewed worries about slowing growth after a weaker‑than‑expected payrolls report.

- In the UK, the Chancellor’s Spring Statement was largely overshadowed by geopolitical developments. The OBR cut its 2026 growth forecast to 1.1% (previously 1.4%). Despite the broader risk‑off mood, energy and defence stocks outperformed, with RELX and Sage also among a small group of positive movers.

- Across Europe (ex‑UK), equities fell more than 7%. Eurozone inflation came in at 1.9% year‑on‑year, and the surge in oil prices amplified near‑term inflation worries, contributing to heightened volatility.

- Japanese equities declined over 6% as investors assessed the implications of higher oil prices for Japan’s energy‑dependent economy. BoJ Governor Ueda warned of potential economic risks from the conflict while reaffirming readiness to raise rates if inflation holds. The yen continued to weaken, prompting officials to hint at possible FX intervention.

- In China and Hong Kong, markets also moved lower as investors balanced geopolitical uncertainty with Beijing’s newly reduced GDP growth target of 4.5%–5%, and its ongoing policy emphasis on technology self‑sufficiency and investment‑driven domestic demand.

Navigating Geopolitical Uncertainty

The current conflict is unfolding in a fundamentally different way from previous episodes. Unlike last year’s brief 12‑day flare‑up, today’s situation involves wider US and Israeli military action and a far more forceful response from Iran. This has included direct strikes on regional energy infrastructure by both sides, such as oil refineries and LNG facilities.

Compounding the risks, the Strait of Hormuz, one of the world’s most vital energy supply routes, is effectively closed. This narrow and exposed passage carries around 20% of global oil and LNG flows, along with significant volumes of fertiliser and aluminium. Any sustained disruption would therefore ripple across multiple commodity markets, not just crude oil.

Financial markets are therefore likely to remain volatile in the very near term as events in the Middle East continue to unfold. That said, history shows that the market impact of geopolitical shocks is often temporary and can at times offer attractive entry points for long‑term investors and some of the best days in equity markets have historically followed material declines.

We continue to closely monitor oil prices and geopolitical events: A prolonged conflict, raising the prospect of persistently higher oil prices, would heighten concerns about inflation becoming more firmly entrenched and tighter monetary policy. However, history suggests it would take a significant and sustained surge in prices to create stagflation.

Other factors like corporate earnings remain strong: We continue to advocate staying invested, maintaining diversification, and focusing on long‑term objectives as markets navigate the current bout of uncertainty.

The value of investments and the income from them can go down as well as up and you could get back less than you invested. Past performance is not a reliable indicator of future performance.

The content of this article is not intended to be or does not constitute investment research as defined by the Financial Conduct Authority. The content should also not be relied upon when making investment decisions, and at no point should the information be treated as specific advice. The article has no regard for the specific investment objectives, financial situation or needs of any specific client, person, or entity.