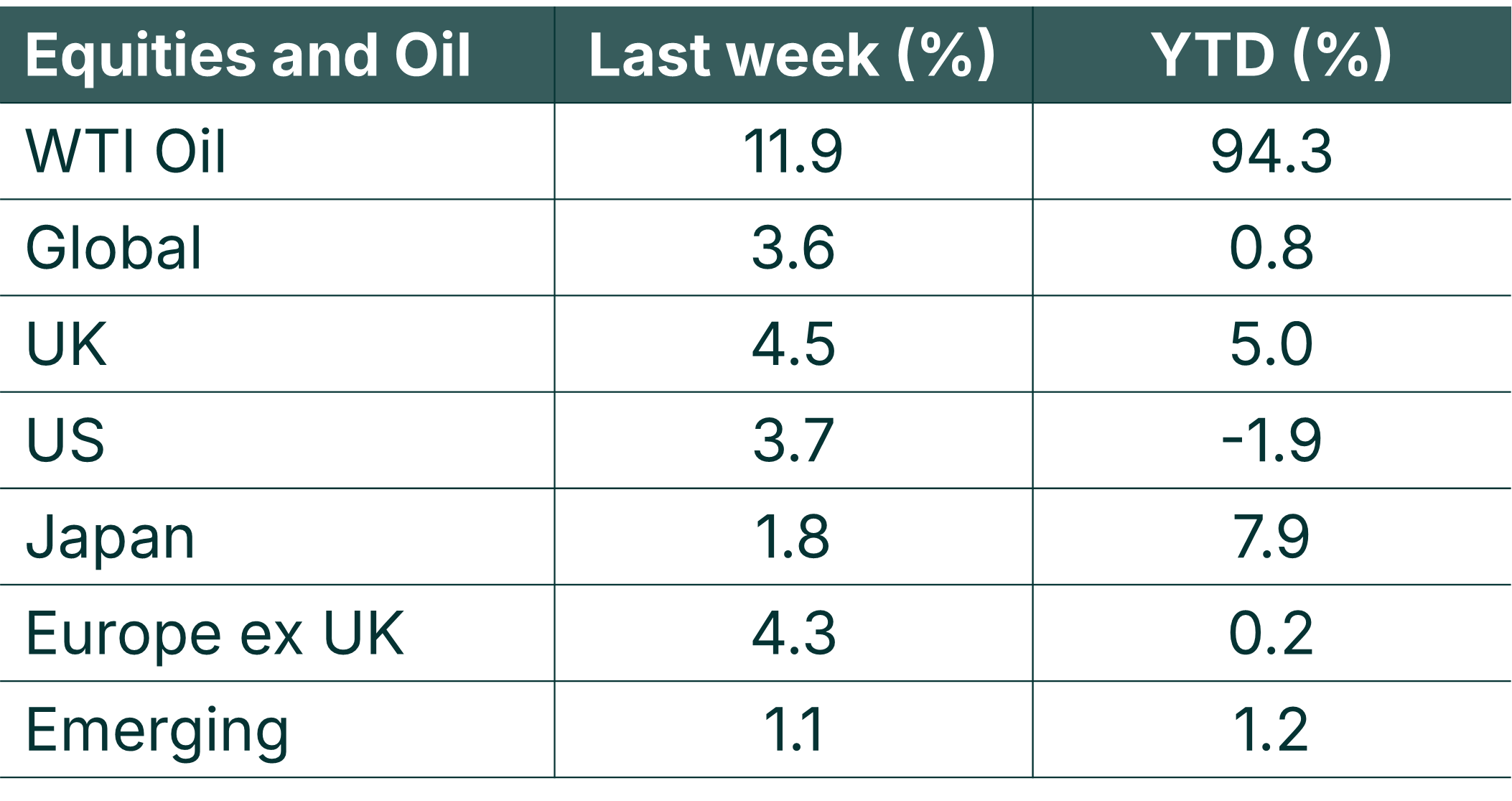

Investment markets posted good gains last week, with both bonds and equities rallying on hopes of a de-escalation to the Iran conflict. UK stocks fared best, driven by strong gains from the mining and banking sector. US economic data also came in strong last week, with the monthly jobs number posting its best reading since December 2024.

This week the focus will remain on the Iran conflict, with 8pm (US Eastern time) 7th April being President Trump’s latest deadline for Iran to reopen the Strait of Hormuz.

Source: Bloomberg. Currency GBP.

Last week

- Stock markets posted strong gains on hopes that the Iran conflict might be reaching a conclusion.

- UK stocks did particularly well, with large companies within the index faring best.

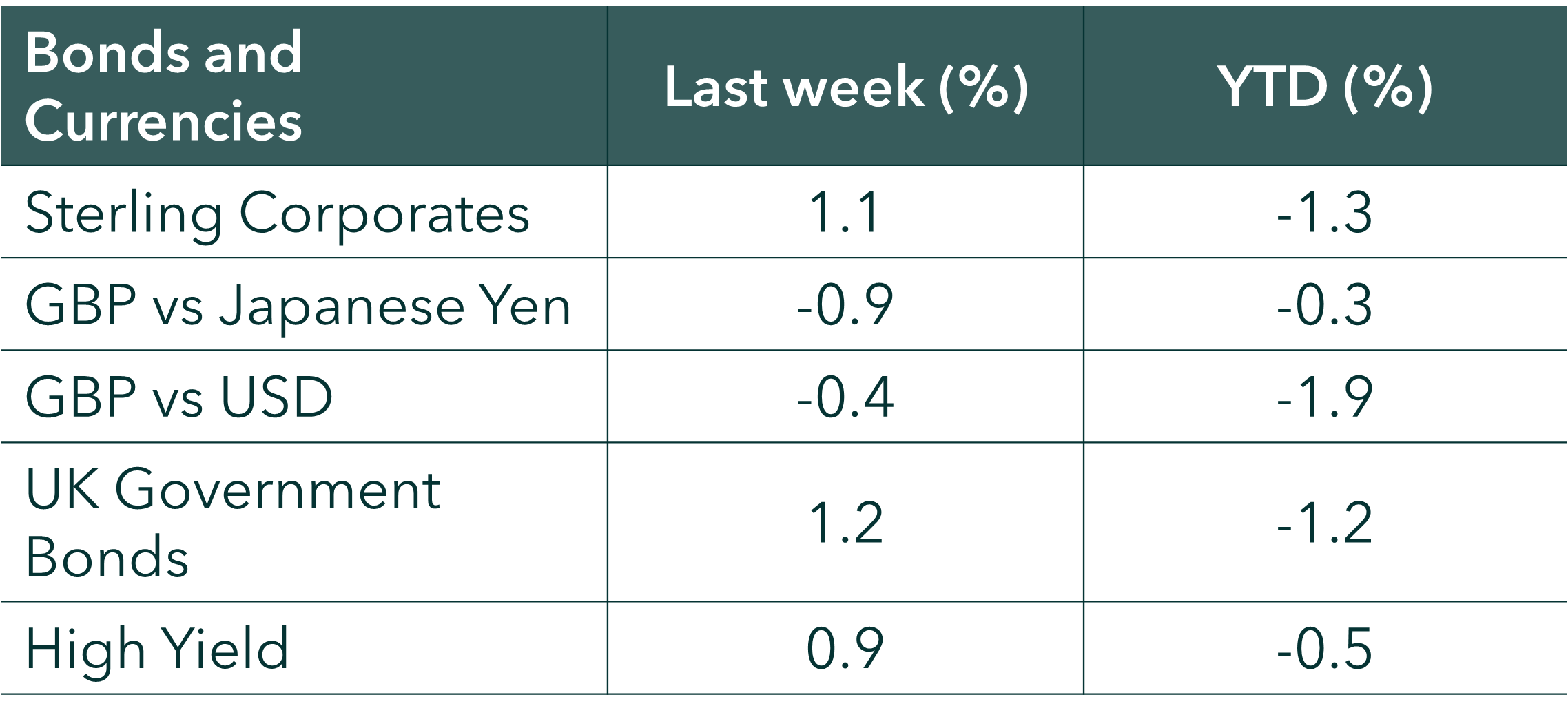

- Bond markets rallied as yields fell on expectations of lower than feared longer-term inflation and on less tightening from Central Banks.

- The US Dollar rose (as has been the case for much of the conflict) – which helped boost returns on US assets for Sterling investors.

- US economic data came in strong, with the jobs market bouncing back after a weak reading in February.

This week

- The Iran war will remain front and centre of investors’ attention this week.

- Alongside that, we have US inflation data (CPI is expected to come in at 3.4%) and the start of US earnings season, with Exxon and Shell both reporting. Analysts (as per Factset) are expecting Q1 2026 earnings for US companies to grow at 13.2% YoY. If this comes to pass, this would represent the 6th consecutive quarter of double-digit earnings growth for the index – earnings are the key driver of long-term stock returns.

More detail

- Stock markets posted strong gains last week on hopes that the Iran war may be reaching an end. Global stock markets rose by 3.6% on the week, with gains for UK investors being helped by US Dollar strength. The US Dollar has risen about 2.5% vs the Pound since the conflict began which has served to soften the blow of losses in US stocks (which dominate the global benchmark).

- Messaging has been mixed from President Trump as to when a ceasefire or de-escalation may occur. At time of writing, President Trump has issued Iran with a deadline of 8pm on 7th April to re-open the Strait of Hormuz. As Magnus noted in their 6 for ’26 article, geopolitical events and intra-year declines are an unfortunate feature of markets. Sticking with a plan and staying invested is the best approach in these markets as the best returns often follow the worst days. Last year was a good example of this, with returns for US stocks in the 15-month period to end March 2026 being c10% in price terms, but just 0.4% if one missed out on the returns from the best trading day (source: Ritholtz).

- UK stock markets enjoyed the biggest bounce back last week and much of this was due to gains in the larger stocks within the index. The Utilities sector rose by over 7.5%, benefiting from falling bond yields, whilst the Materials and Banking sectors were both up over 6% on the week. The UK banking sector has been amongst the hardest hit within the UK share index, having fallen about 18% since its end February highs. The sector now trades on 8.4x forward earnings vs the broader UK market on 12.3x forward earnings.

- Bond yields fell last week which meant that bond prices rose. In the UK, government bonds (10 yr) returned about 1.2% on the week as inflation expectations fell along with expectations for interest rate hikes from the Bank of England. The bond futures markets are now pricing in 2 interest rate hikes in the UK for the remainder of 2026. Whilst this is less than the 3.5 interest rate hikes that they were pricing in on 20th March (post the Bank of England’s meeting), it is still a long way from the 2 further interest rate cuts that were being priced at end February. The uncertainty around the duration of the conflict is the key driver here.

- US economic data came in strong last week, with the monthly jobs number (nonfarm payrolls) showing 178,000 jobs had been added in March – the best number since December 2024 and significantly higher than the 65,000 number that had been expected. Although this is a great number at a headline level, it is worth noting that it was inflated by health care workers coming back off strike and that it came alongside a decrease in people within the labour force, as well as a reduction in job openings.

- Eurozone inflation rose to 2.5% in March, up from 1.9% in February. This marked the highest rate in over a year and was due in no small part to the 4.9% rise in energy costs.

The value of investments and the income from them can go down as well as up and you could get back less than you invested. Past performance is not a reliable indicator of future performance.

The content of this article is not intended to be or does not constitute investment research as defined by the Financial Conduct Authority. The content should also not be relied upon when making investment decisions, and at no point should the information be treated as specific advice. The article has no regard for the specific investment objectives, financial situation or needs of any specific client, person, or entity.