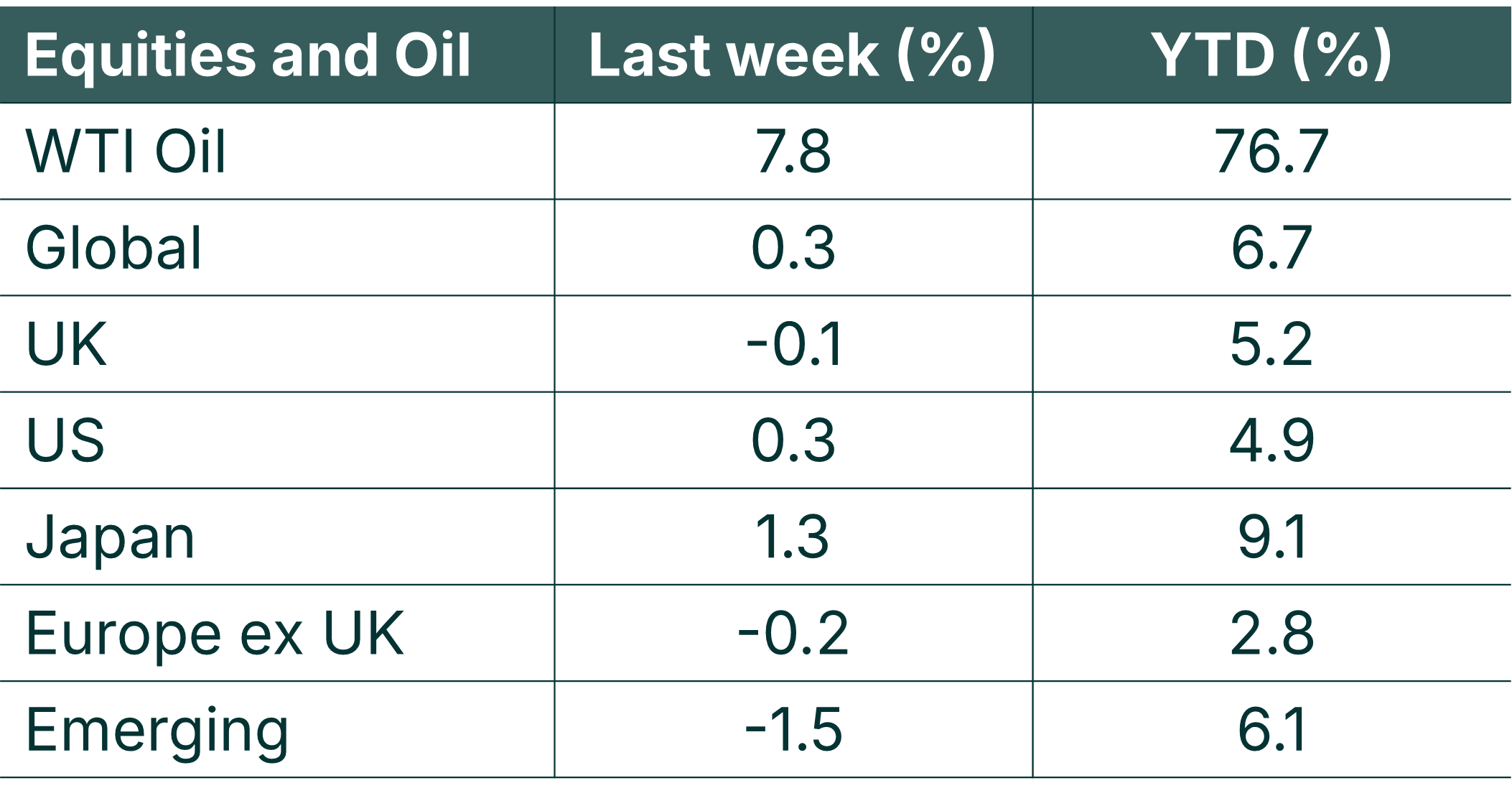

Global stock markets posted modest gains last week to round off an excellent month of April which saw them rise by over 7% – their best month since July 2022!

Last week was dominated by earnings reports from US companies, which continued to come in strong and evidenced continued spending on AI infrastructure. Alongside that, last week saw the Bank of England and the US Federal Reserve meet, with interest rates kept on hold.

This week sees several US and UK companies release earnings figures as well as the much-watched US monthly jobs data – due out on Friday.

Last week

- Global stock markets posted modest positive gains, closing out an excellent month of April

- US technology companies continued to report very strong earnings

- Central Banks kept interest rates on hold

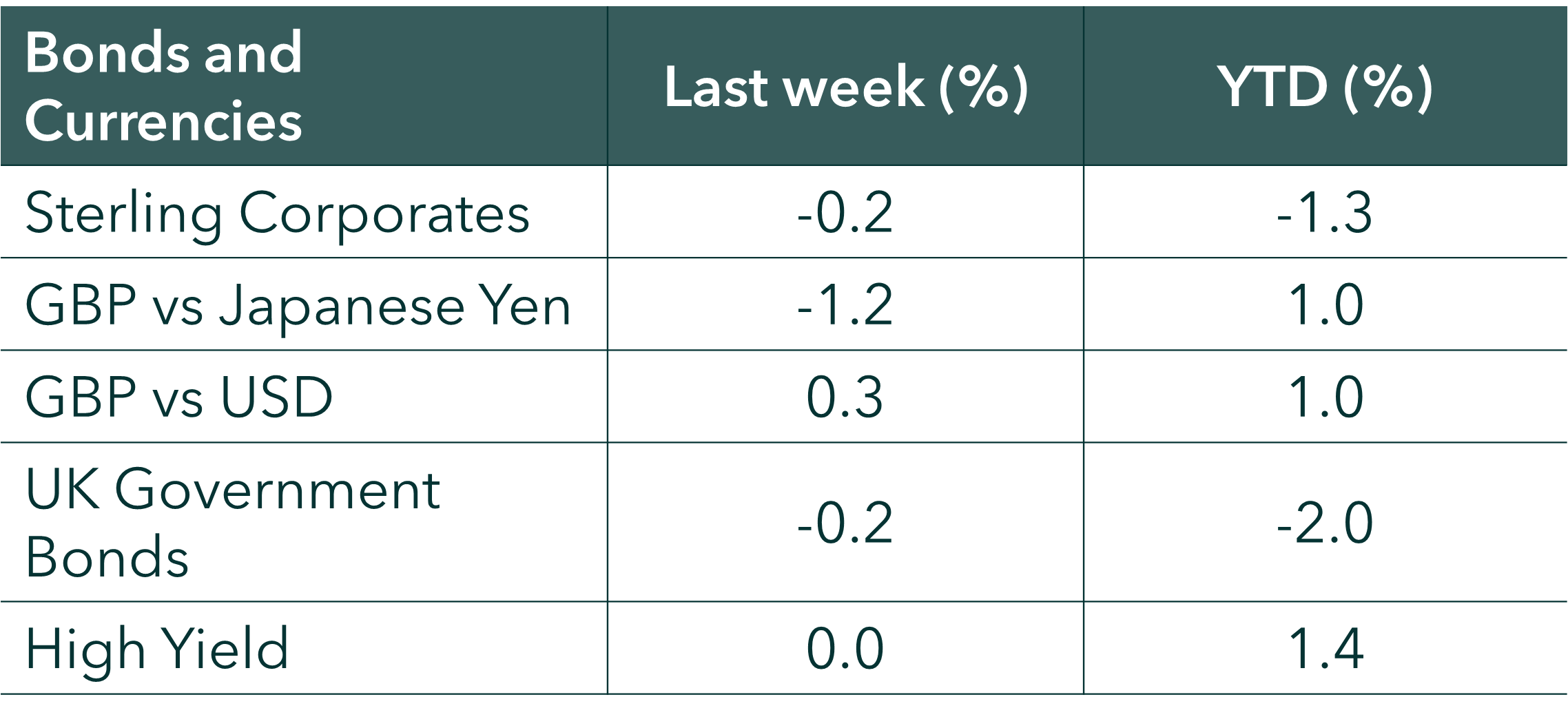

- Bond markets posted modest losses as yields rose

Next week

- It’s a relatively quiet week on the economic and corporate data front

- US companies Disney, Uber and McDonald’s report their earnings

- UK companies HSBC, Shell, Next and Diageo all release figures

- US jobs data on Friday will be keenly watched as always

More details

Global stocks posted modest gains last week, rounding off a strong month of April which saw them rise by 7.4% – their best month since July 2022. Much of the gain in the month came from the US share market which rose by 7.5%. The US share market constitutes c70% of the global share market and hence is always a key driver of return.

US Technology shares have been the biggest driver of growth in the US share market over the month of April. Technology accounts for c35% of the US share index and the US tech sector rose by 14.3% in the month of April – making for its best month since November 2002! Much of the gain came from Semi-Conductors (with this sub-index up 24% in April), with gains being driven by strong earnings off the back of increased AI demand.

Corporate earnings were front and centre last week, with big US tech dominating. We are almost two thirds of the way through US earnings season (with 63% of companies having reported as at 2/5/26) and US companies are growing their earnings at a blended growth rate of 27.1%. This is significantly higher than the 13.1% growth rate that had been pencilled in by analysts (as per Factset data) at 31st March 2026 and puts us on course for the 6th consecutive quarter of double-digit earnings growth in the US.

The technology sector in the US has grown its earnings by a rate of 50% year-over-year over the course of the first quarter of 2026 and is expected to grow earnings by c40% for the full calendar year of 2026. This helps explain the very strong share price performance in the month of April. From a valuation perspective, the sector is trading on a 12-month forward price/earnings multiple of about 24x – which is less than its 5 year average (of 25.8) and about half the valuation that it traded on headed into the dot.com crash in 99/2000.

Increased demand for AI infrastructure is evidenced with the increased capital expenditure targets from the big US tech companies and has also been a driver of emerging markets – notably South Korea (c18% of the EM index weight), and companies such as Samsung and SK Hynix. Last week’s earnings reports from Microsoft, Alphabet, Meta and Amazon saw them increase their capex budgets for this year, with the group expected to spend north of $680bn this year to fuel their AI buildouts.

Central Banks met last week and kept interest rates on hold amidst uncertainty around the knock-on effects of the Iran War.

The US Federal Reserve held rates at 3.75% in an 8-4 vote; making for the largest number of dissents since 1992. 3 of these dissents were on board with the rate decision (i.e. to hold) but not with leaving an “easing bias” in the accompanying policy statement, one of the dissents was in favour of a rate cut. Fed Chair Powell said that he would remain on the Fed’s Board of Governors for an undetermined period, with his term as a Central Bank Governor running through to January 2028.

The Bank of England also kept interest rates on hold at 3.75%, in an 8-1 split vote. The Bank of England adopted 3 economic scenarios (A, B & C) in place of their usual inflation forecast, with most members attaching most weight to scenario B which has CPI inflation at 3.7% at year-end.

The European Central Bank kept rates on hold at 2% and the Bank of Japan kept rates steady at 0.75% but signalled further tightening.

Government bond markets gave up some ground last week, with UK gilts closing out the week down 2% for the year-to-date. The 10-year UK Government bond yield ended last week with a yield of 4.96%, having closed above 5% on 29th April – its highest closing level since summer 2008.

The value of investments and the income from them can go down as well as up and you could get back less than you invested. Past performance is not a reliable indicator of future performance.

The content of this article is not intended to be or does not constitute investment research as defined by the Financial Conduct Authority. The content should also not be relied upon when making investment decisions, and at no point should the information be treated as specific advice. The article has no regard for the specific investment objectives, financial situation or needs of any specific client, person, or entity.