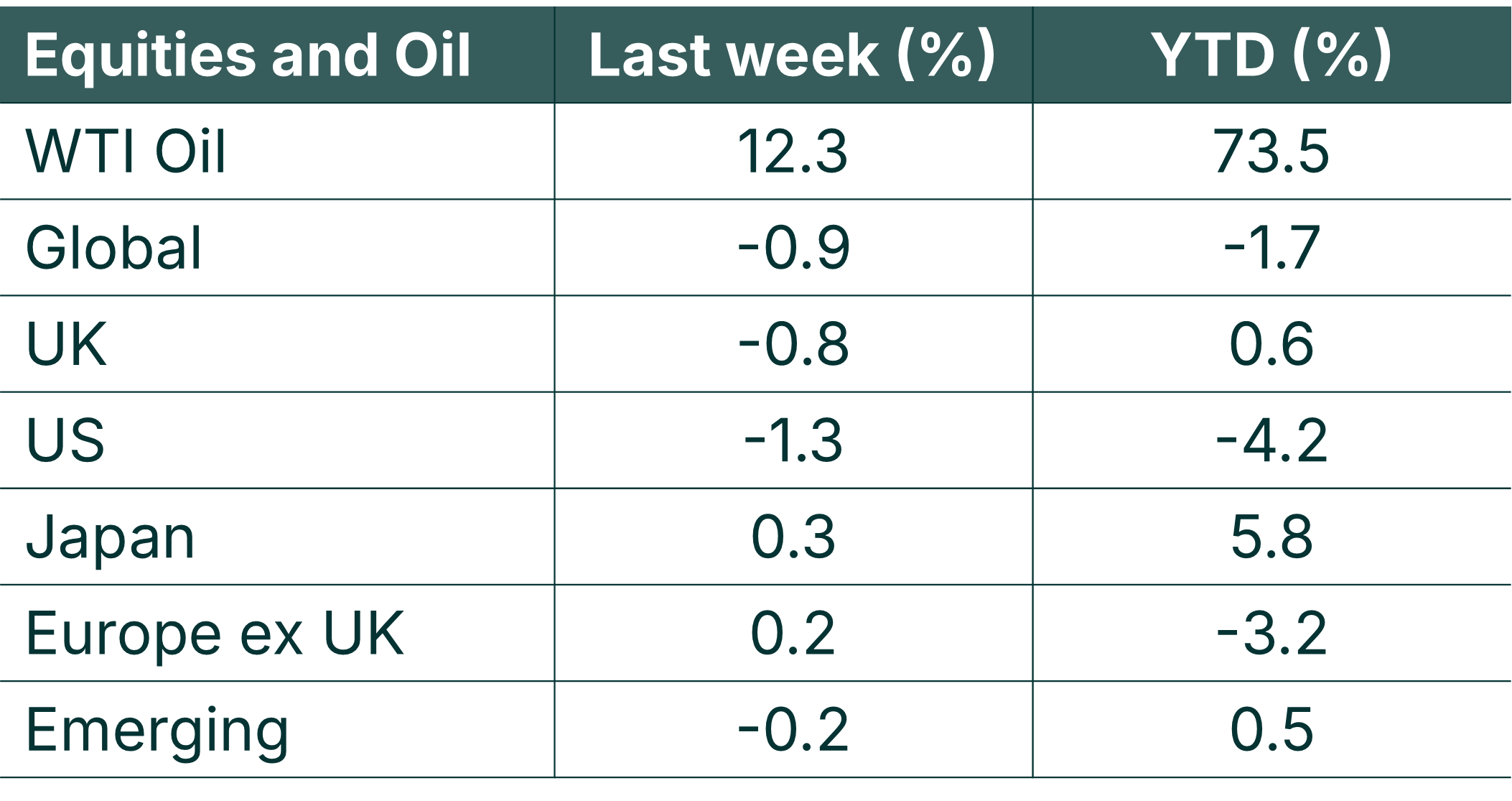

Markets are beginning to show a clear divergence between commodities and financial assets. Global equities declined 0.9% over the week and remain negative year-to-date, with both the US and Europe underperforming. Japan is the notable outperformer among developed markets, while the UK and emerging markets have posted modest positive returns.

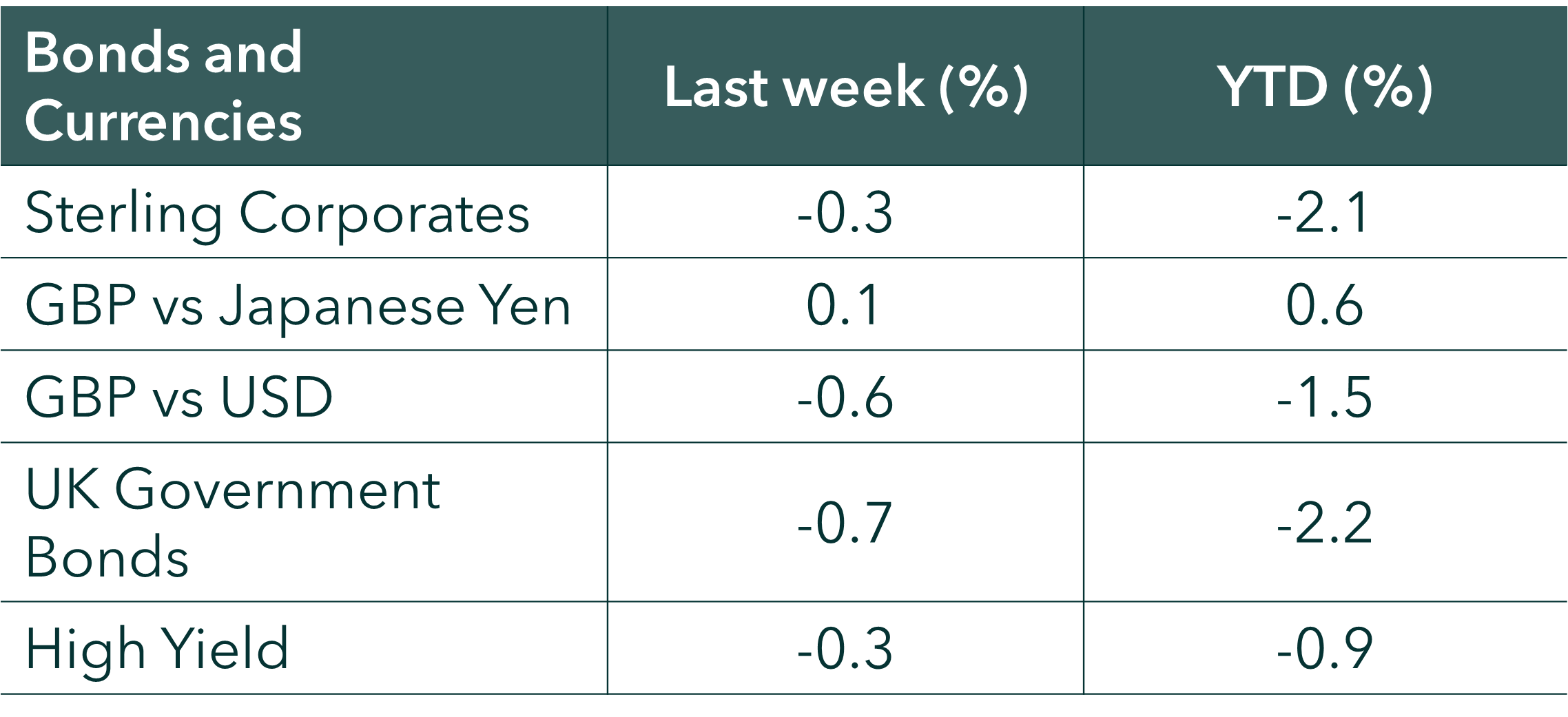

Fixed income continues to face headwinds from higher yields, with UK gilts and sterling corporate bonds both down over 2% year-to-date. However, high yield has shown relative resilience, declining just 0.9% since the start of the year.

In currency markets, sterling has strengthened against the yen but weakened versus the US dollar, reinforcing the broader theme of USD strength.

Source: Bloomberg. Currency GBP.

Last week

- We received the UK inflation data last Tuesday and it was exactly as expected at 3%, but the numbers were moot given that the prices had all been collected and processed before the conflict started.

- We saw UK reports from Kingfisher (retail / housing exposure), who delivered 6% profit growth, supported by resilient UK demand (like-for-like sales 3.3%), offsetting weaker European performance. The guidance was slightly ahead of expectations which suggested some pockets of strength in UK consumer and trade activity.

- In contrast Asda (consumer discretionary / grocery) who reported a 30% decline in earnings, this was in part driven by its aggressive price cutting regime to regain market share and from operational disruption from IT restructuring.

- The earning flow was relatively light in the US, however Lululemon Athletica reported modest results, with its Q4 revenue up just 1% and full-year growth of 5%. This indicated a potential slowdown in discretionary demand and more cautious consumers.

This week

- The US Jobs report and manufacturing surveys are due this week will help give some early indication of how households and businesses are weathering higher energy prices, as well as help markets calibrate the impact on corporate earnings and outlook for interest rates.

- We are expecting US Earnings reports expected next week from companies including Nike (NKE), McCormick (MKC) and ConAgra Brands (CAG).

More detail

- The US markets posted a 1.3% loss this week, marking its fifth consecutive weekly loss and putting the market benchmark on track for its largest monthly loss in three and a half years. The declines have come amid the US-Israel war with Iran, which has contributed to market uncertainty and a surge in oil prices. Communication services experienced the largest weekly drop in the sectors, falling 7.2%, followed by a 3.5% decline in technology and a 2.1% slip in financials. Consumer discretionary, industrials, health care and real estate also moved lower. On the upside it was the defensive parts of the market that moved with energy jumping 6.2%, followed by a 4.2% rise in materials and a 2.9% advance in utilities. Consumer staples also edged up 1.2%.

- The OECD also published its interim economic outlook. It is the first major report published since the start of the conflict detailing growth forecasts across the developed markets. The revisions were most pronounced in Europe and the UK. The UK stands out as the weakest performer, with growth reduced to around 0.7% from approximately 1.2%, reflecting heightened sensitivity to external shocks and weaker underlying momentum. Similarly, Germany and France have seen notable downward revisions, consistent with their exposure to energy costs and cyclical industrial sectors. In contrast, the US is the only major economy showing an upward revision, with growth expectations increasing to circa 2.0%. This divergence likely reflects stronger domestic demand and relative insulation from energy price shocks, potentially linked to its position as a net energy exporter. Japan appears broadly stable, with only marginal changes to its outlook.

- In fixed income markets, higher inflation expectations have driven a repricing of UK rates. The recent 10-year gilt auction cleared at a yield of 4.91%, the highest since 2008, with solid demand indicating investors require greater compensation rather than signaling reduced appetite for UK debt. Markets have shifted to pricing in further Bank of England tightening this year, reversing prior expectations for rate cuts.

The value of investments and the income from them can go down as well as up and you could get back less than you invested. Past performance is not a reliable indicator of future performance.

The content of this article is not intended to be or does not constitute investment research as defined by the Financial Conduct Authority. The content should also not be relied upon when making investment decisions, and at no point should the information be treated as specific advice. The article has no regard for the specific investment objectives, financial situation or needs of any specific client, person, or entity.