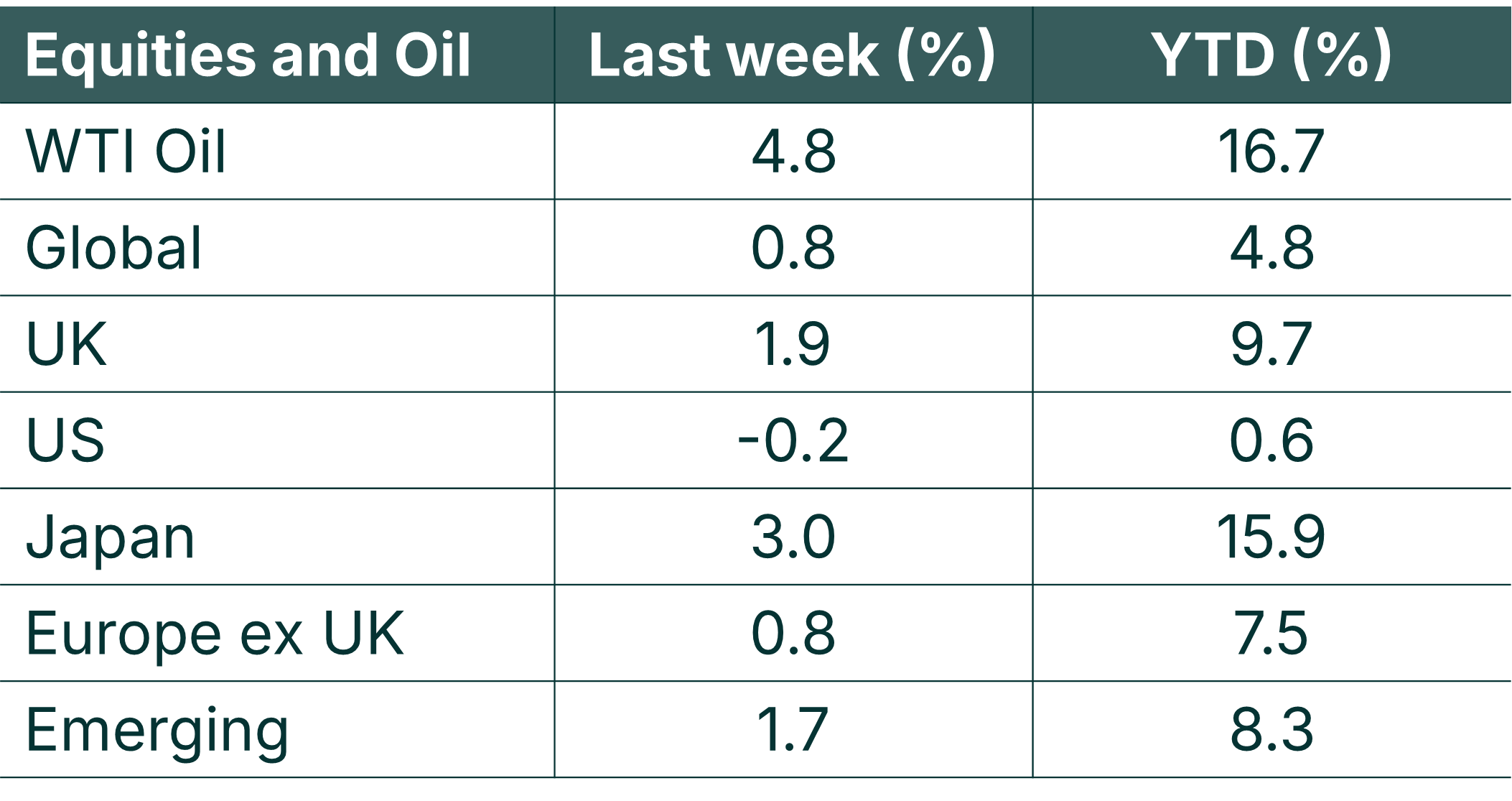

Following the geopolitical escalation in the Middle East, WTI Oil rose 4.8% over the week and nearly 16% year-to-date. This was due to the US air strikes on Iran and subsequent Iranian response in the region which has the potential to disrupt the oil supply through the Strait of Hormuz.

In the other news Japanese equities delivered solid gains, up 3% on the week and 15.9% so far this year. In contrast, US equities fell 0.2% and remain broadly flat year-to-date, continuing their relative underperformance versus other developed and emerging markets. This highlights the degree of regional dispersion we are seeing in 2026.

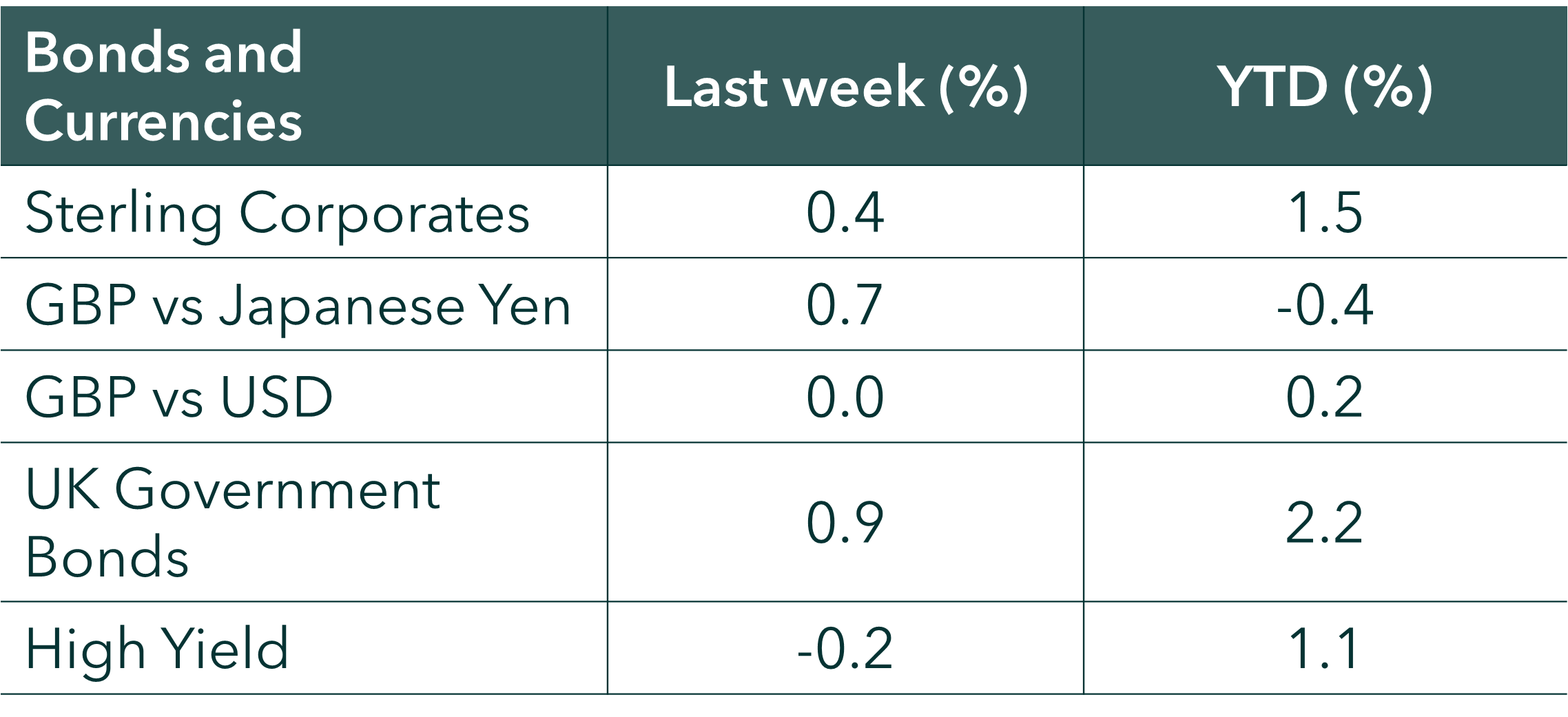

Bond markets were steady. UK Government bonds gained 0.9% on the week and are now up 2.2% year-to-date, while corporate bonds also posted modest gains. High yield was slightly negative over the week but remains positive for the year. Currency moves were limited overall, although Sterling strengthened against the Japanese Yen.

Last week

- Nvidia beat revenue and guidance expectations decisively, but shares fell 5% as investors questioned the sustainability of AI-driven demand.

- Moody’s highlighted $662 billion of off-balance-sheet data centre liabilities across major technology firms.

- Novo Nordisk shares dropped 16% after its latest drug CagriSema trailed Eli Lilly’s Zepbound in the latest clinical trials.

This week

- As the fourth quarter earnings season comes to an end, only a handful of companies remain, including Broadcom, JD Sports Fashion, and Costco Wholesale.

- In the US, the economic calendar is packed with the February jobs report, ISM PMI surveys, and January retail sales.

- In the UK, the key economic event next week is Chancellor Rachel Reeves’s spring statement on Tuesday, where she will present the latest forecasts from the Office for Budget Responsibility.

Source: Bloomberg. Currency GBP.

More detail:

- The weekend we have seen a dramatic shift in the Middle East security landscape following Operation Epic Fury. This was a series of coordinated U.S. and Israeli air strikes targeting Iranian leadership and military infrastructure. It also resulted in an Iranian response, which included missile and drone strikes against regional targets.

- Geopolitical shocks tend to trigger short-term volatility; however, the scale and persistence of the impact depend largely on energy markets. The key risk is the potential disruption around the Strait of Hormuz. This is a narrow shipping channel between the Iranian coast and Oman’s Musandam Peninsula. It is key route for Oil, liquefied natural gas (LNG), fertilisers and industrial metals from the Middle East to the rest of the world.

- Past episodes of Middle East escalation have triggered risk-off behaviour. This is where investors move from speculative assets and pile into “safe havens.” This is often characterised by a dramatic surge in assets that thrive during geopolitical instability. We can expect oil majors and Defense contractors to benefit from this increase instability. Conversely, the “risk-on” sectors are facing a contraction, with airlines and hospitality expected to bear the brunt of the fallout.

In other news

- Nvidia delivered another exceptional set of results, yet the shares declined 5% on the day. Fourth-quarter revenue reached $68.1 billion, up 73% year-on-year and $2 billion ahead of consensus. Guidance for the current quarter came in at $78 billion, roughly $6 billion above expectations. Despite this, investors appeared focused on the durability of demand and the sustainability of capital expenditure trends across hyperscalers, prompting profit-taking after a prolonged rally.

- Moody’s highlighted $662 billion of off-balance-sheet data centre liabilities across major technology firms. According to the report, Amazon, Meta, Alphabet, Microsoft and Oracle collectively hold $969 billion in future lease commitments, with around two-thirds not fully reflected on balance sheets under current GAAP treatment. Moody’s noted that the total equates to roughly 113% of the group’s combined on-balance-sheet debt and suggested this could warrant adjusted leverage metrics in credit analysis. The issue underscores the scale of AI-related infrastructure commitments embedded within the sector.

- In healthcare, Novo Nordisk disappointed investors after trial data showed its next-generation obesity treatment, CagriSema, delivered 23% weight loss after 84 weeks, compared with 25.5% for Eli Lilly’s Zepbound. Shares fell 16% on the news and remain significantly below their 2024 peak. Shortly afterwards, Novo announced US price reductions of up to 50% from January 2027 for Wegovy and Ozempic, bringing monthly pricing to $675. The combination of competitive pressure and pricing adjustments weighed on sentiment towards the obesity franchise.

The value of investments and the income from them can go down as well as up and you could get back less than you invested. Past performance is not a reliable indicator of future performance.

The content of this article is not intended to be or does not constitute investment research as defined by the Financial Conduct Authority. The content should also not be relied upon when making investment decisions, and at no point should the information be treated as specific advice. The article has no regard for the specific investment objectives, financial situation or needs of any specific client, person, or entity.