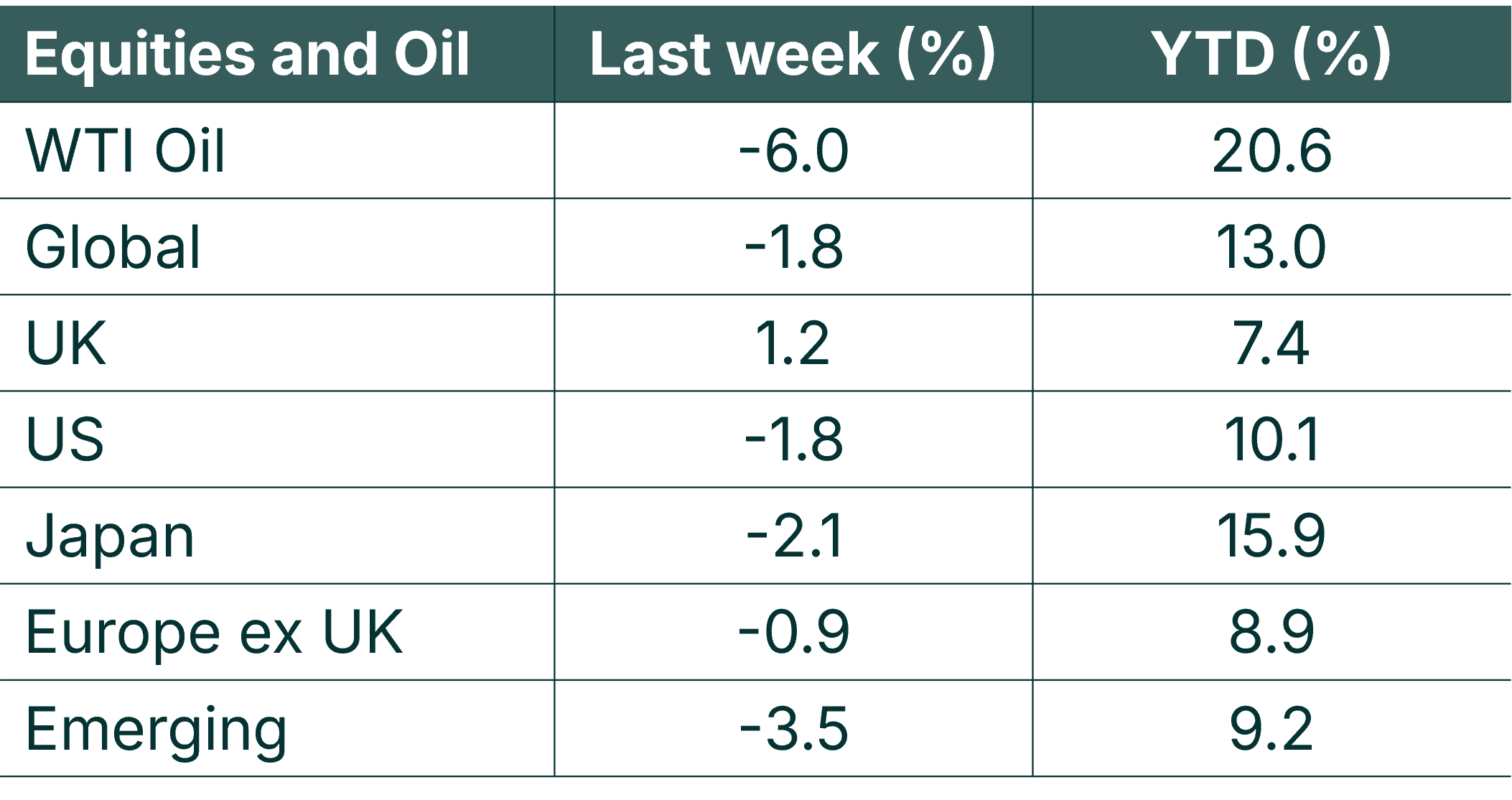

Oil prices fell sharply last week, with WTI down 6.0%, as Middle East supply concerns eased and shipping through the Strait of Hormuz normalised, though this should be considered relative to WTI’s strong year-to-date gains of 20.6%.

UK equities were the standout performer among major markets, rising 1.2% while most other regions declined, dragged lower by weakness in AI and semiconductor stocks. Fixed income provided some stability, with UK government bonds and sterling corporates both posting modest gains.

As we enter the second half of 2026, markets are grappling with a “higher-for-longer” interest rate narrative, a pausing of the AI rally, and the prospect of a pivotal US jobs report next week.

Last week

- WTI Oil fell 6.0% as Middle East tensions eased with some normalization to shipping through the Strait of Hormuz shipping, while Brent crude fell to a four-month low.

- UK equities rose 1.2%, the only major market to post a positive return, supported by its defensive and energy sector characteristics.

- US equities declined, with AI and semiconductor stocks selling off.

- UK government bonds and sterling corporate bonds provided ballast, returning 0.8% and 0.6% respectively, while high yield was flat.

- Micron Technology delivered strong earnings reinforcing AI-driven memory demand, though this was insufficient to prevent broader semiconductor weakness; On Semiconductor announced a circa $7 billion acquisition of Synaptics in one of the week’s largest M&A deals.

This week

- The US June nonfarm payrolls report will be a key event on Thursday, with investors watching closely to Chair Kevin Warsh’s speech for validation of the “higher-for-longer” interest rate narrative.

- US consumer confidence data will also be released, adding further colour to the economic outlook.

- Central bankers gather at the ECB’s Sintra forum, where any shift in tone on rates or inflation will be closely scrutinised.

- Nike reports earnings, among other major consumer companies, providing an early read on consumer spending trends.

- Oil market developments will remain in focus — falling energy prices could feed through to inflation relatively quickly, with implications for rate expectations.

- The AI investment theme continues to evolve, with capital expenditure announcements and earnings commentary likely to drive sentiment in technology stocks following last week’s sharp sector sell-off.

Source: Bloomberg. Currency GBP.

More details

- Market sentiment last week was shaped by three intersecting themes: a reassessment of interest rate expectations, a pause in the AI rally, and a sharp fall in oil prices.

- On rates, the Federal Reserve’s decision to hold steady on 18 June was widely anticipated, but the Fed speeches and commentary last week struck a more hawkish tone. So far this year, markets have shifted from pricing in imminent rate cuts to contemplating the possibility of rates increasing. Treasury yields remained elevated as a result, and this backdrop weighs on risk assets more broadly, particularly high-growth technology stocks whose valuations are sensitive to the discount rate.

- The AI theme, which has been a dominant driver of equity markets through the first half of 2026, showed signs of fatigue last week. Semiconductor and AI-related stocks led US indices lower as investors took profits following an extraordinary run. Emerging concerns around memory-related cost inflation and the scale of AI infrastructure spending added to the caution. Micron’s strong results, which reinforced the robustness of AI-driven memory demand, were notable but not enough to arrest the broader sector weakness. Apple and Microsoft also attracted attention after raising prices on some hardware products, citing rising component and AI infrastructure costs. The central question investors are now asking is whether AI-related capital expenditure has temporarily run ahead of earnings expectations.

- The sharp fall in oil prices was a notable counterpoint to this cautious mood. WTI declined over the week as fears over Middle East supply disruptions eased and shipping through the Strait of Hormuz showed signs of normalisation. While lower energy prices offer some relief on the inflation front, the speed at which this feeds through to headline inflation figures, and in turn to central bank thinking, will be a key watch point in the coming weeks.

- The UK’s relative outperformance stood out against a difficult week for global equities. While UK equities remain the weakest year-to-date performer among the major regions tracked at 7.4%, the market’s composition, with its higher weighting towards energy, financials and more defensive sectors, appeared to offer support during a week characterised by rotation away from high-momentum technology names. Whether this marks the beginning of a more sustained period of UK catch-up remains to be seen.

- Looking ahead, the US June nonfarm payrolls report will be the dominant focus, acting as a potential catalyst for either confirming or challenging the market’s current “higher-for-longer” rate assumption. Central bank discussions at the ECB’s Sintra forum add another layer of interest, particularly for European rate and currency markets.

The value of investments and the income from them can go down as well as up and you could get back less than you invested. Past performance is not a reliable indicator of future performance.

The content of this article is not intended to be or does not constitute investment research as defined by the Financial Conduct Authority. The content should also not be relied upon when making investment decisions, and at no point should the information be treated as specific advice. The article has no regard for the specific investment objectives, financial situation or needs of any specific client, person, or entity.