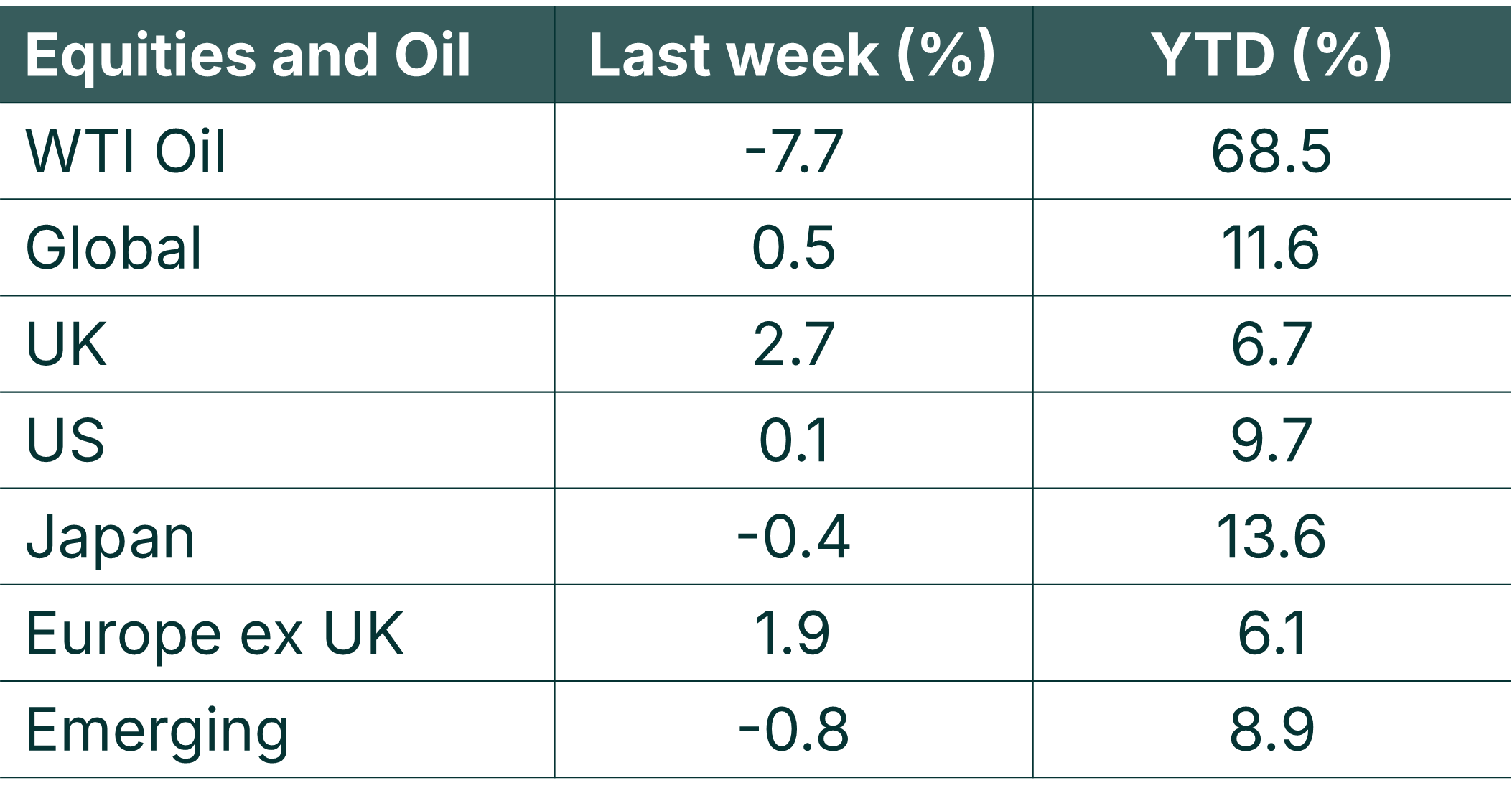

Global and US equities made modest progress last week in Sterling terms, but momentum was strongest in the UK and Europe. This was driven by a significant decline in oil prices and growing optimism around US/Iran peace talks, which was supportive for both the inflation and interest rate outlook.

Over the long weekend, negotiations have continued, with some encouraging developments. Notably, Iran has reopened international internet access after a nearly three-month blackout, signaling a potential easing of domestic restrictions and engagement with the outside world.

Reports suggest a memorandum of understanding between Iran and the US is on the table, which could include a 60-day ceasefire extension, the reopening of the Strait of Hormuz, and a framework for further negotiations on Iran’s nuclear ambitions, the thorniest issue to resolve. While no formal agreement has been reached, the constructive tone of talks supported market sentiment, with Asian equities rising on 25 May in response to the progress made.

Last week

- UK equities gained 2.7% with stocks exposed to international earnings and defence linked stocks like Rolls Royce continuing to perform well. Financials also made headway.

- The S&P 500 hovered near all-time highs, driven by robust corporate earnings and continued enthusiasm for artificial intelligence (AI) stocks but made less headway than the UK and Europe.

- Nvidia delivered another exceptional quarter, with revenues up 85% and profits more than tripling, reinforcing continued strength in AI demand. However, a muted share price reaction following the earnings release reflects growing concerns around possible future competition.

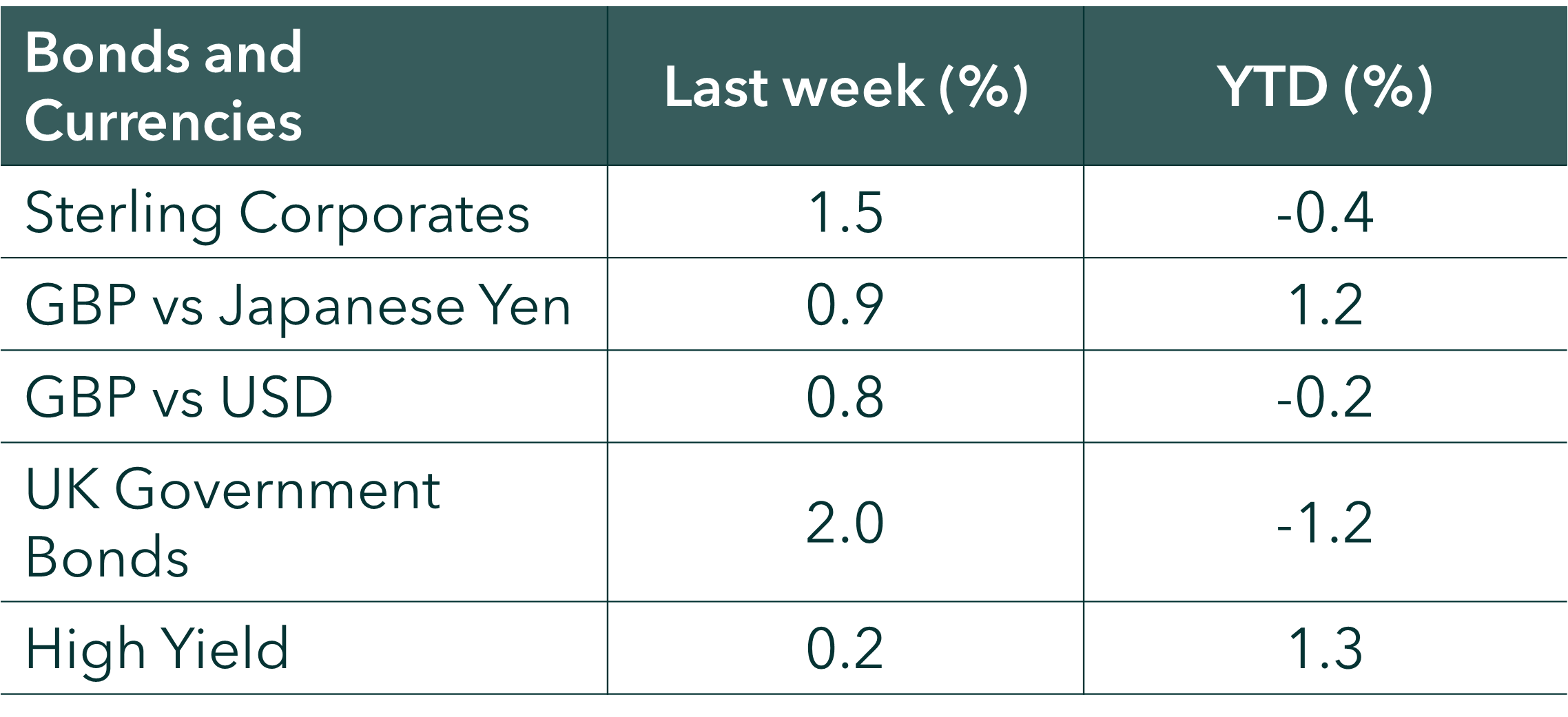

- WTI oil prices fell nearly 8% – which is positive news for the inflation and interest rate outlook and drove a 1.5% increase in the Sterling Corporates index.

This week

- A short week for UK, US, Hong Kong and South Korean markets due to bank holiday closure on Monday.

- The stock market goes into the last week of May with the S&P 500 around the 7,500 mark as earnings season for this quarter ends with Dell and some major retailers set to report.

- Japanese CPI data to be released on Tuesday – this will be indicative of how hawkish interest rate policy moves might be.

- The US personal consumption expenditures price index, the Fed’s preferred measure of inflation, will be released on Thursday.

Source: Bloomberg. Currency GBP.

More details

- Economic data was mixed for the UK and US last week. Once again proving that the economy does not equal the market as we saw some headway in global, US and UK equity indices.

- US economic data showed modest growth: manufacturing strengthened, services softened, but inflation pressures picked up sharply alongside falling employment. However, consumer sentiment fell to a record low, reflecting cost-of-living concerns, while housing activity remained subdued amid rising mortgage rates.

- Additionally, Fed minutes reinforced concerns that persistent inflation may require further policy tightening.

- The UK unemployment rate increased unexpectedly to 5% in the three months to March 2026, up slightly from 4.9% in the previous three-month period.

- On the other hand, annual inflation in the UK slowed to 2.8% in April, down from 3.3% in March and lower than the 3% that had been expected. The ONS noted that an energy price cap introduced by the country’s regulator had curbed inflation.

The value of investments and the income from them can go down as well as up and you could get back less than you invested. Past performance is not a reliable indicator of future performance.

The content of this article is not intended to be or does not constitute investment research as defined by the Financial Conduct Authority. The content should also not be relied upon when making investment decisions, and at no point should the information be treated as specific advice. The article has no regard for the specific investment objectives, financial situation or needs of any specific client, person, or entity.