The conflict in the Middle East continued to unsettle markets, with attacks on energy infrastructure driving volatility across both equities and bonds. Central Banks struck a cautious tone, highlighting upside risks to inflation.

The path of markets will depend on the duration of the conflict and the persistence of disruption to energy supply. However, any growth slowdown driven by higher energy prices would be occurring against a backdrop of relatively resilient economic conditions and lower underlying inflation than in previous crises.

Opportunities are beginning to emerge, although we remain mindful of the speed at which markets can move and the risks of reacting too quickly.

Our thoughts remain with all those affected by the conflict.

Last week

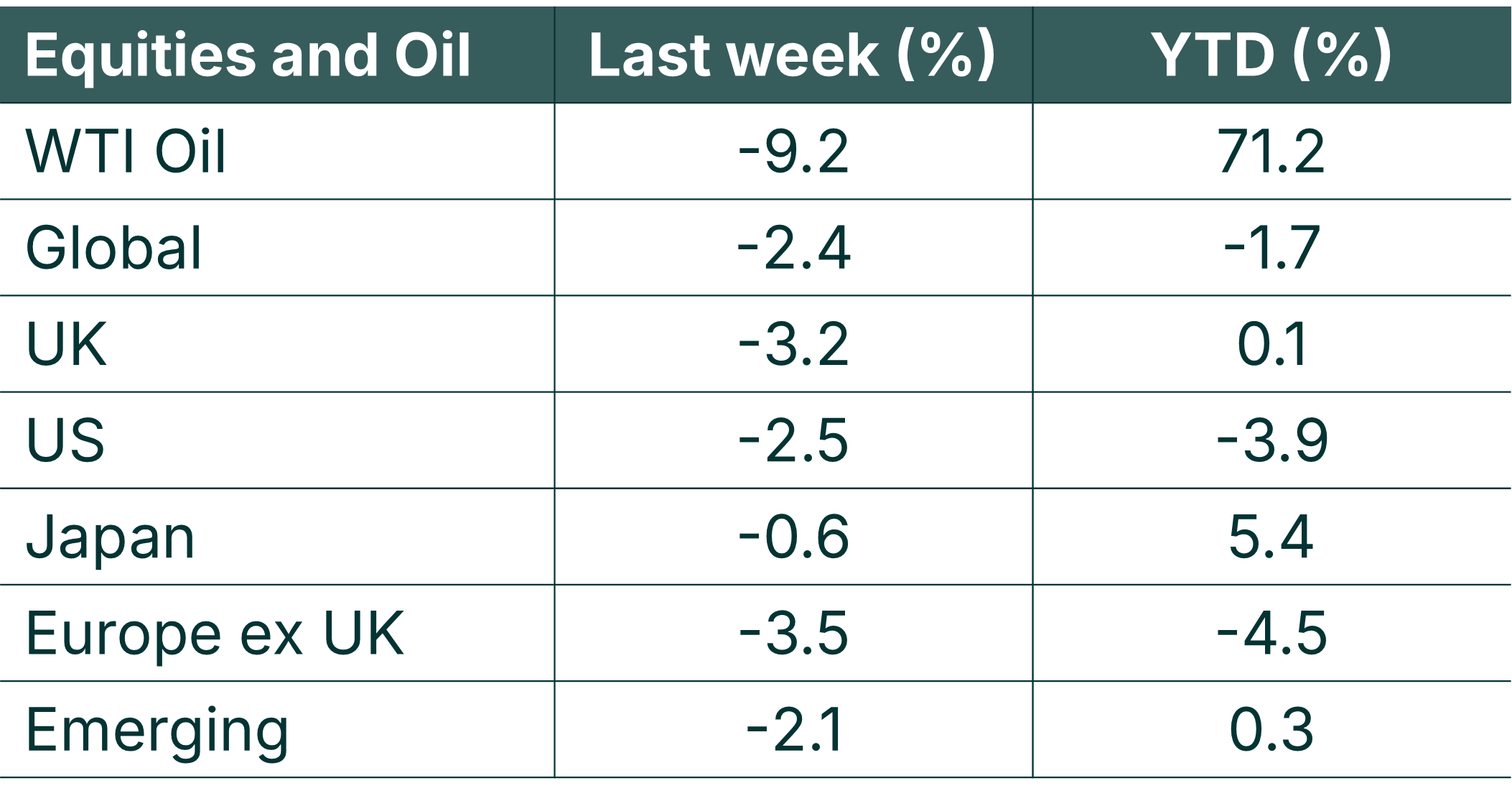

- The conflict in the Middle East remained the primary market driver, with both equities and bonds selling off.

- Central banks kept interest rates on hold.

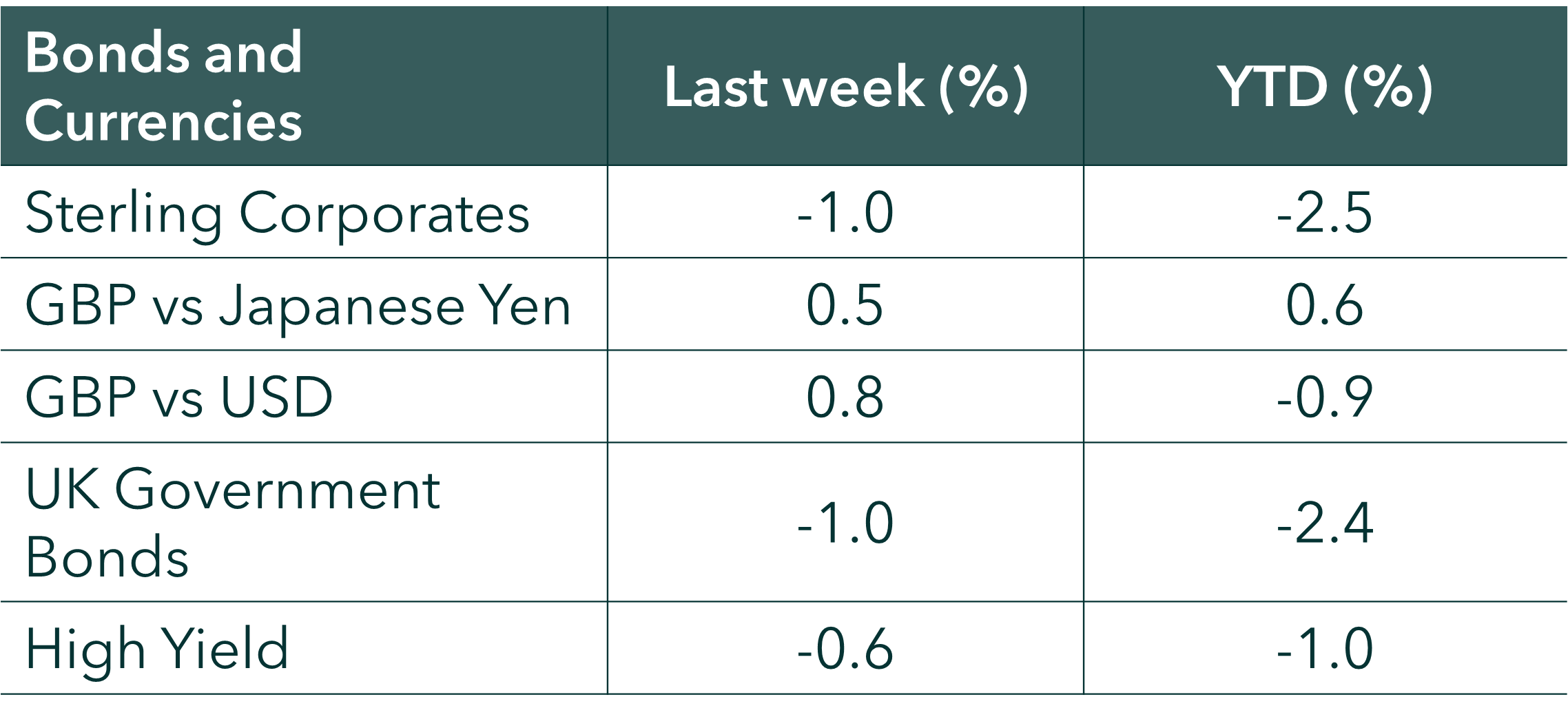

- Bond markets repriced sharply towards interest rate hikes, particularly in the UK.

This week

- The war in the Middle East will remain the key driver of markets.

- UK inflation data (Tuesday) is expected at 3% (Bloomberg consensus). This reflects February data and does not yet capture the recent rise in oil prices.

Source: Bloomberg. Currency GBP.

More detail on Last Week:

- It was another volatile week for markets, with global equities falling for a third consecutive week and moving into negative territory for the year-to-date (down 1.7%). Investor focus remains centred on the likely duration of the conflict.

- While the path of the conflict is uncertain, it is important to remember that long-term equity returns are driven by corporate earnings rather than geopolitical events. Market drawdowns within a year are not unusual: over the past 21 years, global equities have delivered average annual returns of c.10%, despite experiencing average intra-year declines of c.14.5%.

- Recent market weakness has led to a notable de-rating in valuations. Global equities are now trading on 19x forward earnings, with the US at 20.2x (in line with its five-year average). In the near term, markets are likely to be driven more by sentiment than fundamentals, but valuations are becoming more attractive for long-term investors. This is evident in areas such as US technology (c.22.5x 12-month forward earnings) and UK banks (c.8x forward earnings).

- Brent crude oil closed the week at $112 per barrel—elevated, but below the peaks of $128 in March 2022 and $146 in July 2008. The issue is less about overall supply and more about access, which will remain constrained while the Strait of Hormuz is effectively closed.

- Last week saw the US Federal Reserve, the European Central Bank, the Bank of Japan and the Bank of England all meet. All banks kept interest rates on hold.

- The Federal Reserve held rates at 3.75% (upper bound) in an 11–1 vote. This was accompanied by a modest upward revision to growth forecasts (2026 GDP at 2.4%) and inflation expectations (2.7%). Chair Powell indicated he intends to remain in position until the ongoing investigation into the Fed’s headquarters is concluded and a successor—likely Kevin Warsh—is officially confirmed.

- The Bank of England also held rates at 3.75% in a unanimous decision. Governor Andrew Bailey noted that the Bank stands “ready to act” to ensure inflation returns to its 2% target over the medium term. This was interpreted hawkishly by markets, with UK rate expectations shifting materially—from pricing two rate cuts a month ago to three rate hikes for the year. As a result, UK two-year gilt yields rose to 4.56%, while ten-year yields reached 4.99%.

- Movements in bond markets have been pronounced, with UK government bonds now down 2.4% for the year-to-date and down 4.6% so far in March. However, we’d note that longer-term inflation expectations have remained well anchored. Whilst short-term inflation measures have spiked (e.g. 1-year swaps), we would note that longer-term measures have been much more contained. Furthermore, we’d note that credit spreads remain below their 5-year average levels (US credit spreads are 81 basis points, whilst US high yields spreads are 312 basis points) – suggesting that fundamentals remain intact.

The value of investments and the income from them can go down as well as up and you could get back less than you invested. Past performance is not a reliable indicator of future performance.

The content of this article is not intended to be or does not constitute investment research as defined by the Financial Conduct Authority. The content should also not be relied upon when making investment decisions, and at no point should the information be treated as specific advice. The article has no regard for the specific investment objectives, financial situation or needs of any specific client, person, or entity.