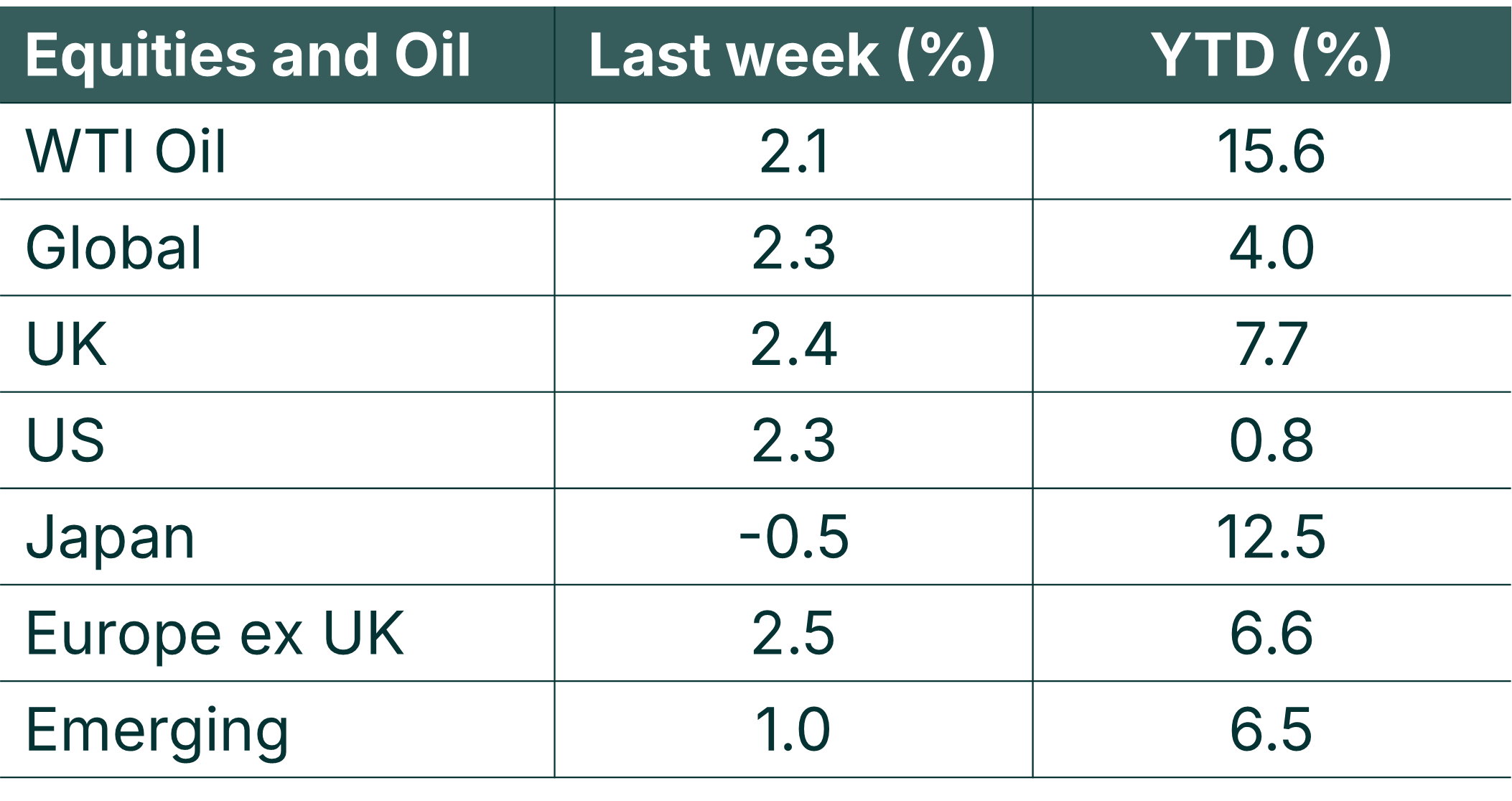

Last week saw strong gains for global share markets, which were further boosted by weakness in the Pound vs the US Dollar. Despite weaker-than-expected UK economic data, UK shares were amongst the best performing: rising by 2.4% on the week which took gains for the year-to-date to 7.7%. This is a great example of the stock market not being equal to the economy, with UK stock markets getting a boost from their sector composition (notably energy) and from boosted expectations for interest rate cuts (to support the economy).

This week is quiet on the economic calendar, but we’d expect attention to be focussed on geopolitics, with US trade policy and tensions with Iran being front of mind.

Last week

- Stock markets had a strong week, with US gains being boosted by weakness in the Pound

- UK share markets did particularly well: benefiting from their high sector allocation to energy and financials

- The US Supreme Court ruled against the emergency trade tariffs which the Trump Administration put in place last year

- UK economic data came in weak: but this was received well by the markets as it paved the way for interest rate cuts.

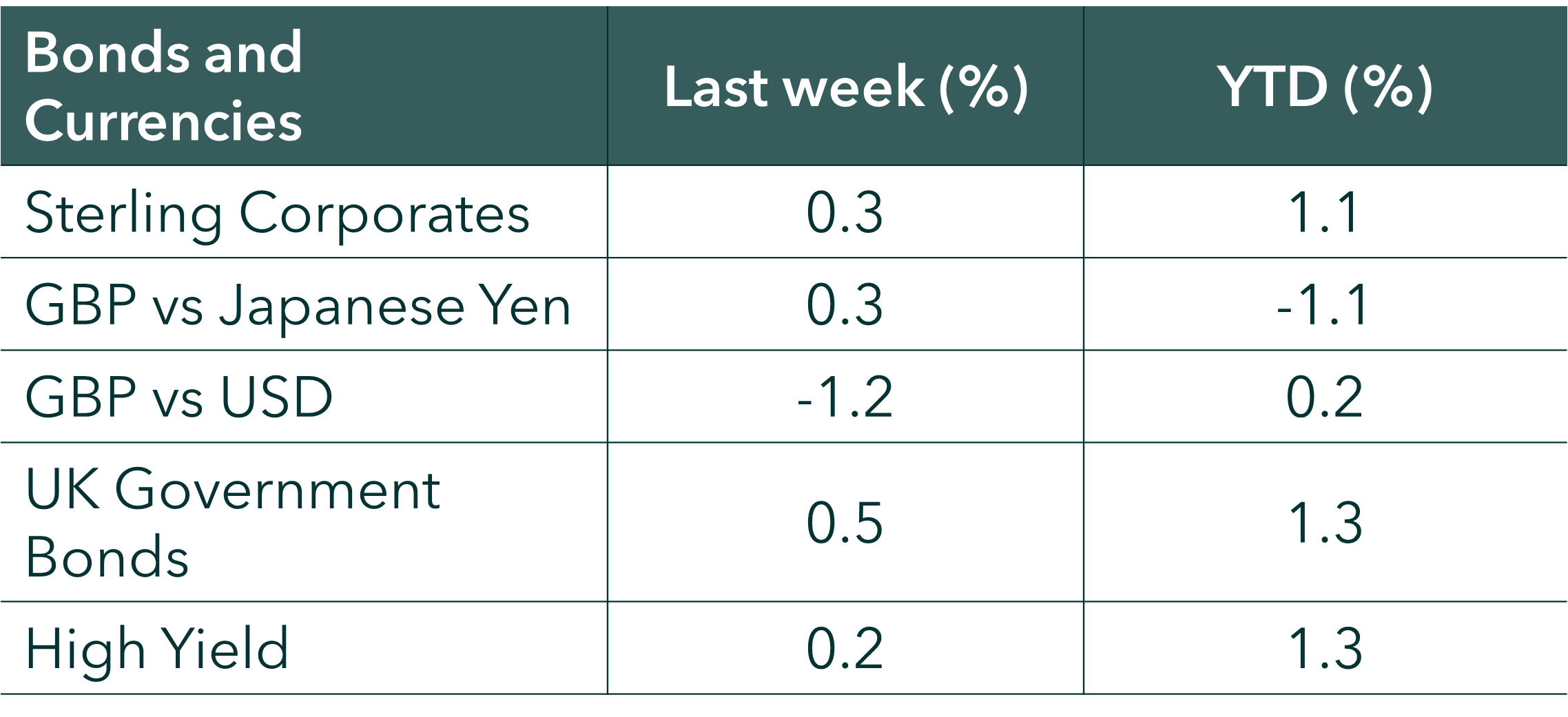

- Bond markets posted modest gains, with UK Government bonds doing particularly well.

This week

- Geopolitics is likely to strongly feature this week, with US trade policy in the spotlight.

- In the US, Nvidia and Salesforce both report their earnings on Wednesday.

- In the UK, there’s a broad mix of companies reporting their results. Standard Chartered report on Tuesday, HSBC on Wednesday, Jupiter, Rolls Royce and London Stock Exchange on Thursday, with Rathbones and Pearson (amongst others) on Friday.

Source: Bloomberg. Currency GBP.

More detail:

- Global stock markets rose by about 2.3% last week, with the US market (which makes up about 70% of the global stock market) helping to boost returns; itself up by 2.3%. Much of the rise in US shares came from the c1.2% rise on the week in the US Dollar vs the Pound. The Pound fell on weaker-than-expected UK economic data which boosted expectations of the Bank of England cutting interest rates at their next meeting (19th March).

- UK share markets did particularly well last week, rising by 2.4%. This rise was helped by the sector composition of the UK share index, with its c8.5% weighting to the energy sector and near 30% weighting to financials. The energy sector got a boost from rising oil prices on the back of escalating tensions between the US and Iran, whilst financials continued their strong run, with the UK banking sector up by over 4.5% on the week.

- Q4 US earnings season is drawing to a close, with c75% of companies having reported their results. Results have been significantly better than expected, with a blended growth rate of 13.2% (as compared to the 8.3% YoY growth rate that had been pencilled in by Analysts – as per Factset – at the end of December 2025). This puts the US share market on course for its 5th consecutive quarter of double-digit earnings growth.

- Friday saw the US Supreme Court strike down the Trump Administration’s trade tariffs that had been introduced under emergency economic powers. President Trump reacted immediately by saying that he would replace the removed tariffs with a 10% levy on all goods coming into the US. He later upped this rate to the 15% maximum rate that is permissible under the Trade Act of 1974. This 15% rate is permissible for a limited period (150 days) under Section 122 of this law.

- UK economic data last week helped pave the way for interest rate cuts. Inflation came in at 3% (from 3.4%), the unemployment rate ticked up more than expected (to 5.2% from 5.1%) and average weekly earnings (wages) came in lower than expected: at 4.2% YoY. This led the bond futures markets to price in an 80% chance of an interest rate cut from the Bank of England at the 19th March meeting, with 2 full interest rate cuts now being priced in for 2026.

- Bond markets rose modestly last week, with UK sovereign bonds doing particularly well (as yields shifted down to reflect increased expectations of interest rate cuts). The week closed out with UK 2-year Government bonds yielding 3.56% and UK 10-year Government bonds yielding 4.35%.

The value of investments and the income from them can go down as well as up and you could get back less than you invested. Past performance is not a reliable indicator of future performance.

The content of this article is not intended to be or does not constitute investment research as defined by the Financial Conduct Authority. The content should also not be relied upon when making investment decisions, and at no point should the information be treated as specific advice. The article has no regard for the specific investment objectives, financial situation or needs of any specific client, person, or entity.