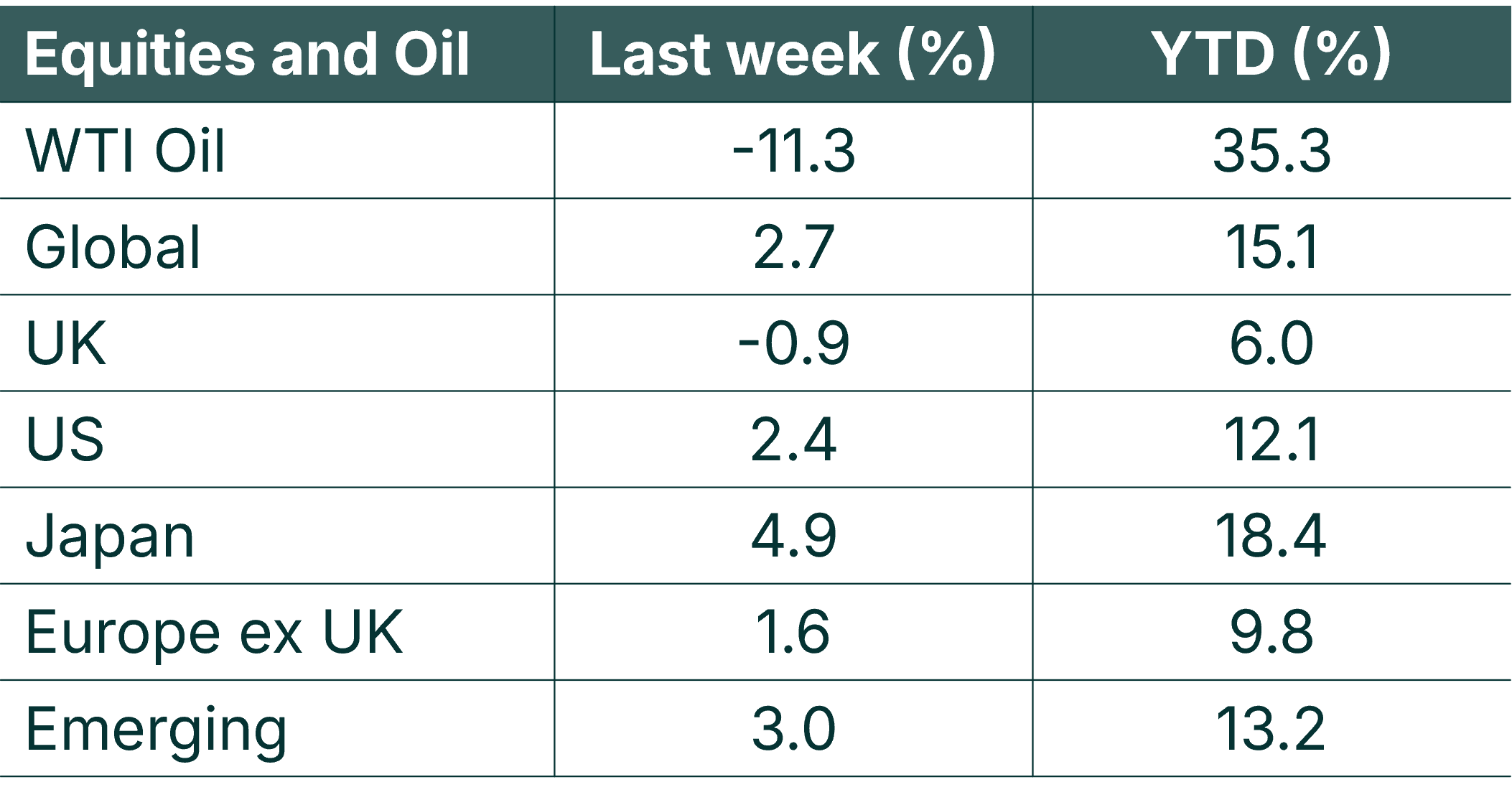

Global markets rose strongly last week as easing tensions in the Middle East helped improve investor sentiment and push oil prices lower. At the same time, technology shares continued to lead markets higher, reflecting continued optimism around AI-related investment and earnings growth.

Whilst the US Federal Reserve and the Bank of England both kept interest rates unchanged, US policymakers struck a slightly more hawkish tone than investors had expected. Bond yields moved higher as markets priced in a higher future path for interest rates, particularly in the United States.

Looking ahead, the economic calendar is relatively light. As a result, markets are likely to remain focused on developments in the Middle East alongside incoming US inflation and business activity data.

Last week

- Global stocks rose with the technology sector powering the rally.

- Easing geopolitical tensions in the Middle East helped support risk assets and reduce pressure on oil prices.

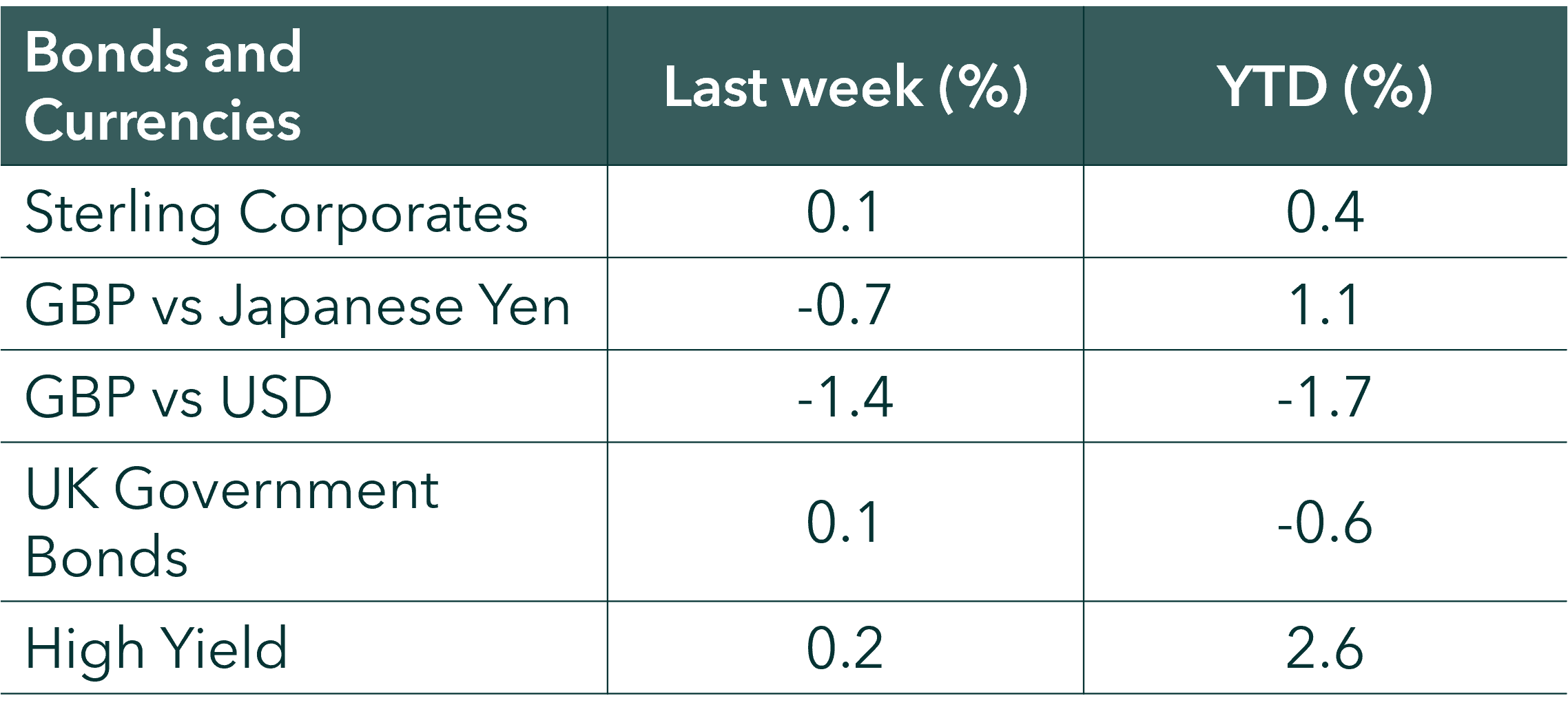

- The Pound fell vs the US Dollar, the Yen and the Euro

- The US Fed and the Bank of England kept interest rates on hold at 3.75%, whilst the Bank of Japan raised interest rates to 1%.

- Short-dated government bond yields rose in both the US and UK, whilst inflation expectations fell, resulting in higher real yields.

This week

- Markets are likely to remain sensitive to geopolitical developments in the Middle East.

- Initial (“flash”) June Purchasing Managers’ Index (PMI) readings are released for Japan, the UK, Germany and the US on Tuesday.

- US Core PCE inflation, the Federal Reserve’s preferred measure of inflation, is released on Wednesday. Economists surveyed by Bloomberg expect a reading of 3.4%.

- Corporate earnings are relatively light, with results due from Babcock on Monday and FedEx and Micron on Wednesday.

Source: Bloomberg. Currency GBP.

More details

- Global share markets rose by approximately 2.6% last week, with a weaker Pound providing an additional boost to returns for UK investors with overseas exposure. Easing tensions in the Middle East helped improve investor sentiment and reduce pressure on oil prices, supporting risk assets globally.

Central banks and bond markets

- Whilst both the Federal Reserve and the Bank of England left interest rates unchanged at 3.75%, policymakers struck a slightly more hawkish tone than investors had anticipated.

- In the United States, the Federal Reserve’s updated Summary of Economic Projections implied a slightly higher future path for interest rates than had been expected in March. Bond futures markets now imply one additional 0.25% interest rate increase relative to expectations a week earlier.

- The Bank of England voted 7-2 to leave interest rates unchanged, with the two dissenters favouring a rate increase. This followed a UK inflation reading of 2.8% for May, below the 3.0% consensus expectation.

- Perhaps the most notable development last week was the rise in real yields. Whilst nominal government bond yields moved higher, inflation expectations fell, meaning investors are now being offered more attractive inflation-adjusted returns.

- US short-dated real yields are now close to 2%, their highest level since October 2024. UK real yields have also risen and are now at their highest level since January.

Technology remains the market leader

- Returns last week were led by the US equity market, which accounts for approximately 70% of global equity indices. The technology sector was again the standout performer, rising 4.8% during the week and leaving the sector up approximately 25% year-to-date.

- Technology now represents nearly 40% of the US equity market and around 30% of the global equity market, meaning sector performance continues to have a significant influence on broader market returns.

- Despite strong recent gains, technology valuations remain relatively reasonable. The US technology sector currently trades on approximately 21.5x end-2027 earnings, only modestly above the broader US market on around 20x.

- Importantly, this valuation remains below both the sector’s five and ten-year average multiples and is less than half the level reached during the dot-com boom of 1999-2000.

Japan posts strongest week since February

- Japanese equities also performed strongly, rising almost 5% and recording their strongest weekly advance since February.

- Technology shares again led the gains, with the Japanese technology sector rising more than 15% during the week.

- The gains came despite the Bank of Japan raising interest rates to 1%, the highest level in 31 years, suggesting investors remain confident that economic growth and corporate earnings can withstand gradually tighter monetary policy.

Sterling weakens

- Sterling weakened during the week, falling approximately 1.4% against the US Dollar and 0.7% against the Japanese Yen. The currency finished the week trading at 1.32 against the US Dollar.

- Most of the weakness occurred following the Federal Reserve and Bank of England policy meetings as investors reassessed the relative outlook for interest rates in the US and UK.

The value of investments and the income from them can go down as well as up and you could get back less than you invested. Past performance is not a reliable indicator of future performance.

The content of this article is not intended to be or does not constitute investment research as defined by the Financial Conduct Authority. The content should also not be relied upon when making investment decisions, and at no point should the information be treated as specific advice. The article has no regard for the specific investment objectives, financial situation or needs of any specific client, person, or entity.