De-escalation in the Middle East, including the ongoing US–Iran ceasefire, led to a further decline in oil prices last week, and supported a broad rally in risk assets. However, while there have been reports of the Strait of Hormuz reopening, access for commercial shipping remains constrained.

A 10-day ceasefire between Israel and Lebanon is currently in place, with US–Iran negotiations ongoing. While tensions have eased, the situation remains fluid. Until a more durable resolution is reached, risks to global growth and inflation persist, keeping central banks cautious.

Source: Bloomberg. Currency GBP.

Last week

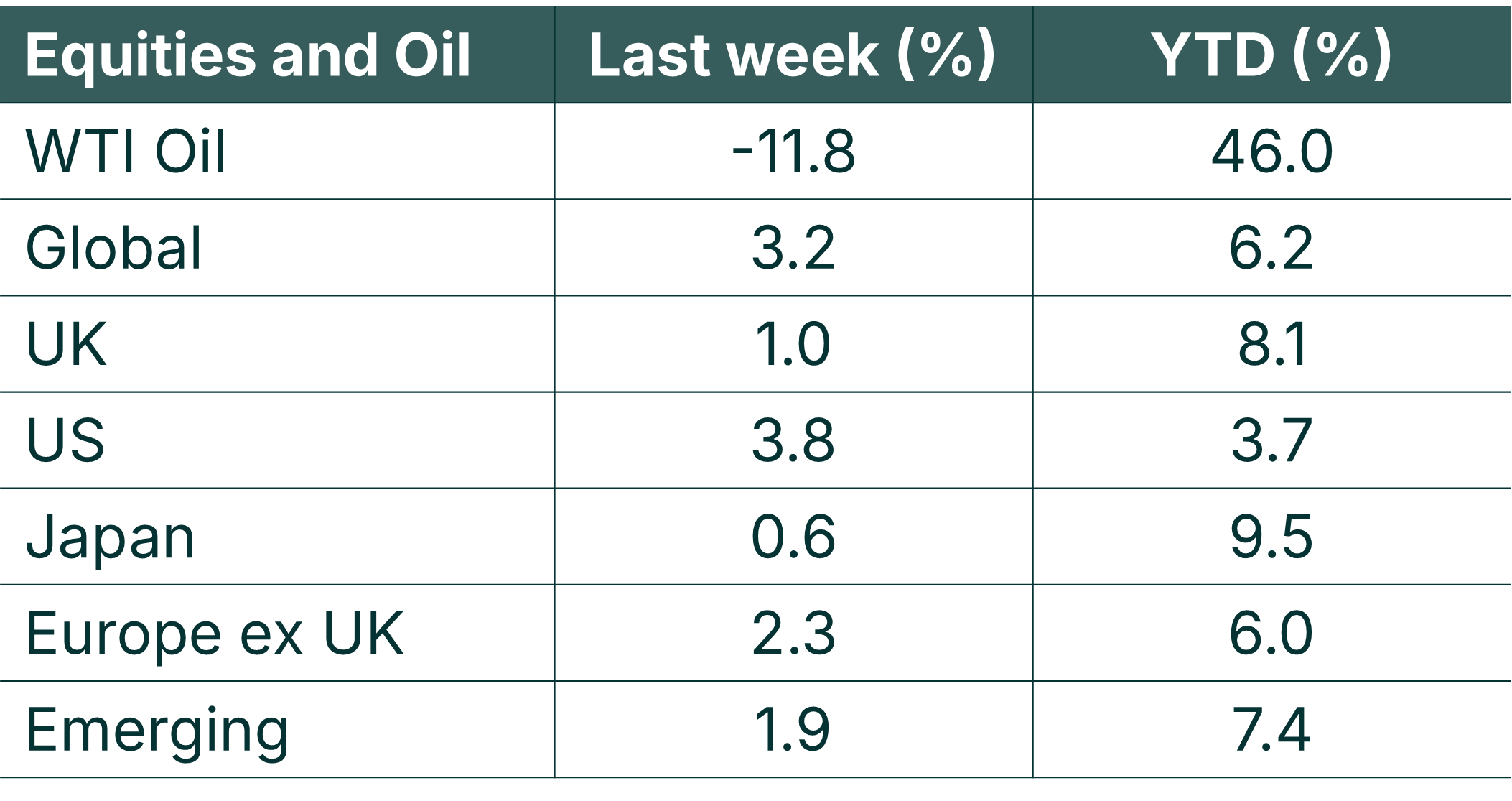

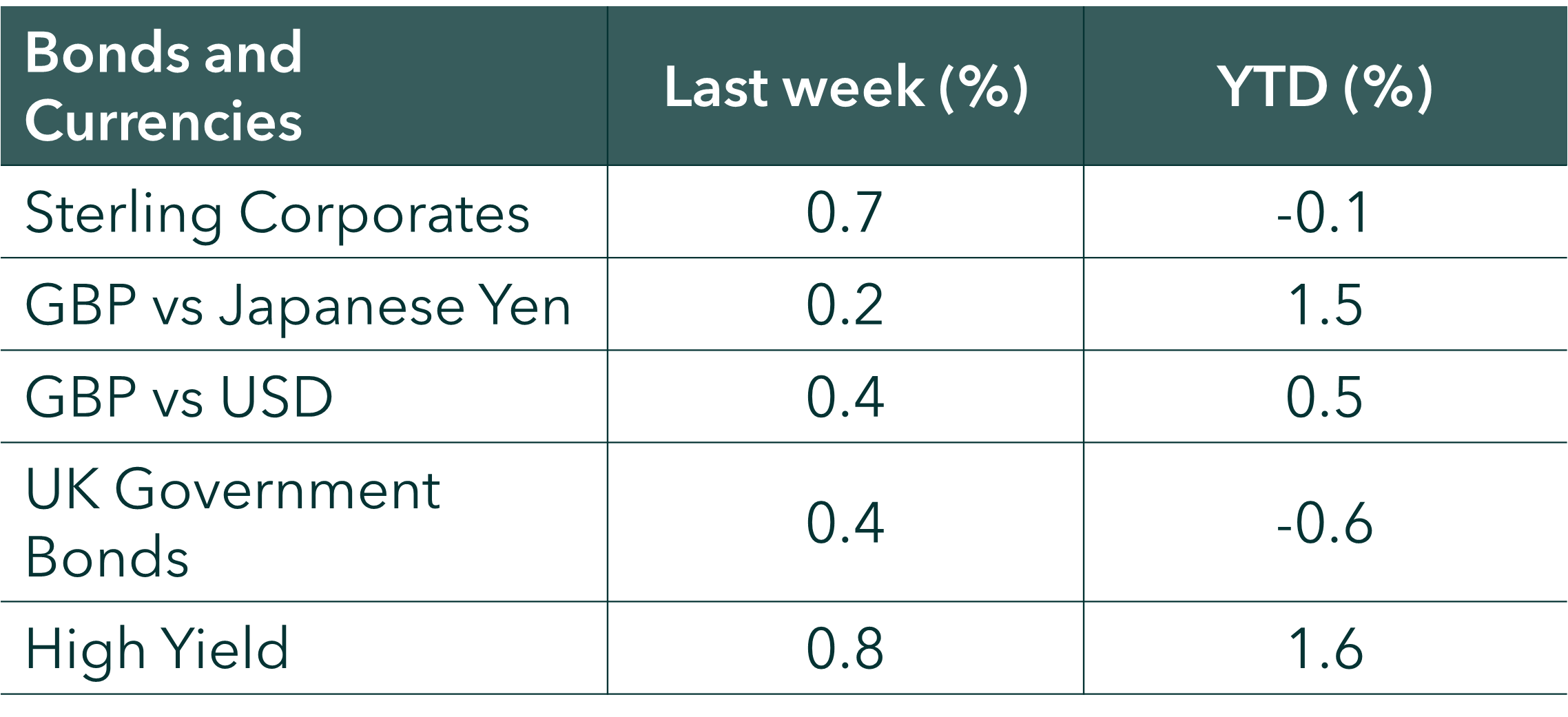

Both equities and bonds delivered positive returns, supported by easing geopolitical tensions and a solid start to Q1 earnings season. Global equities rose by 3.2%, led by the US, up 3.8%, while bond markets also strengthened.

- Earnings season: Early results were encouraging, particularly from notable financials and technology stocks, including the likes of Goldman Sachs, JP Morgan, ASML and TSMC.

- IMF / World Bank: Spring meetings included a modest downgrade to global growth forecasts, alongside discussions on structural themes such as defence spending, AI and cybersecurity.

- China: Data releases showed volatility in trade, with notable shifts in both imports and exports, affecting the trade balance. GDP growth came in slightly ahead of expectations at 5% year-on-year.

- UK: Friday saw the release of February GDP data, which surprised to the upside, at +0.5%, exceeding consensus estimates.

This week

The week ahead will remain busy, with a continued focus on corporate earnings and geopolitics.

- Corporate Earnings: Key names from a good mix of sectors will be reporting, including GE Aerospace, UnitedHealth, Intuitive Surgical and Tesla.

- Geopolitics: Ongoing monitoring of US-Iran negotiations and Israel-Lebanon ceasefire.

- Economic data (backward-looking): A combination of economic data, including US and UK retail sales (March), UK unemployment (February), and inflation data (March) from several major economies.

- Economic data (forward-looking): Flash PMI data for the UK and Eurozone (April), alongside Eurozone economic sentiment indicators (April) are due out.

More detail

- The Q1 earnings season is now well underway, with early financials and large-cap technology reports delivering generally positive results. The focus now broadens across sectors, with market attention on both company guidance and margin resilience. This week’s earnings will provide further insight into how corporates are navigating geopolitical uncertainty, cost pressures and demand conditions. Tesla is likely to attract attention given its position within the “Magnificent 7”.

- The IMF and World Bank discussions highlighted a softer global growth backdrop, while also emphasising longer-term structural challenges, including geopolitical fragmentation and technological disruption (including AI and cybersecurity risks).

- In China, trade balance reflected heightened global uncertainty, with notable fluctuations in both imports and exports. While industrial production came in stronger than expected, weaker than expected retail sales point to uneven domestic demand.

- Upcoming economic data will help assess the extent to which recent geopolitical tensions are feeding through to activity and inflation. Any sustained easing in tensions could support further downside in oil prices and relieve inflationary pressures.

The value of investments and the income from them can go down as well as up and you could get back less than you invested. Past performance is not a reliable indicator of future performance.

The content of this article is not intended to be or does not constitute investment research as defined by the Financial Conduct Authority. The content should also not be relied upon when making investment decisions, and at no point should the information be treated as specific advice. The article has no regard for the specific investment objectives, financial situation or needs of any specific client, person, or entity.