Global equities continued to move higher last week, supported by resilient corporate earnings and steady investor sentiment. Oil markets remained a key focus, with WTI crude oil rising 11% amid renewed concerns over global supply dynamics and ongoing geopolitical tensions.

With earnings season beginning to wind down, investor attention is now shifting towards macroeconomic data releases and geopolitical developments.

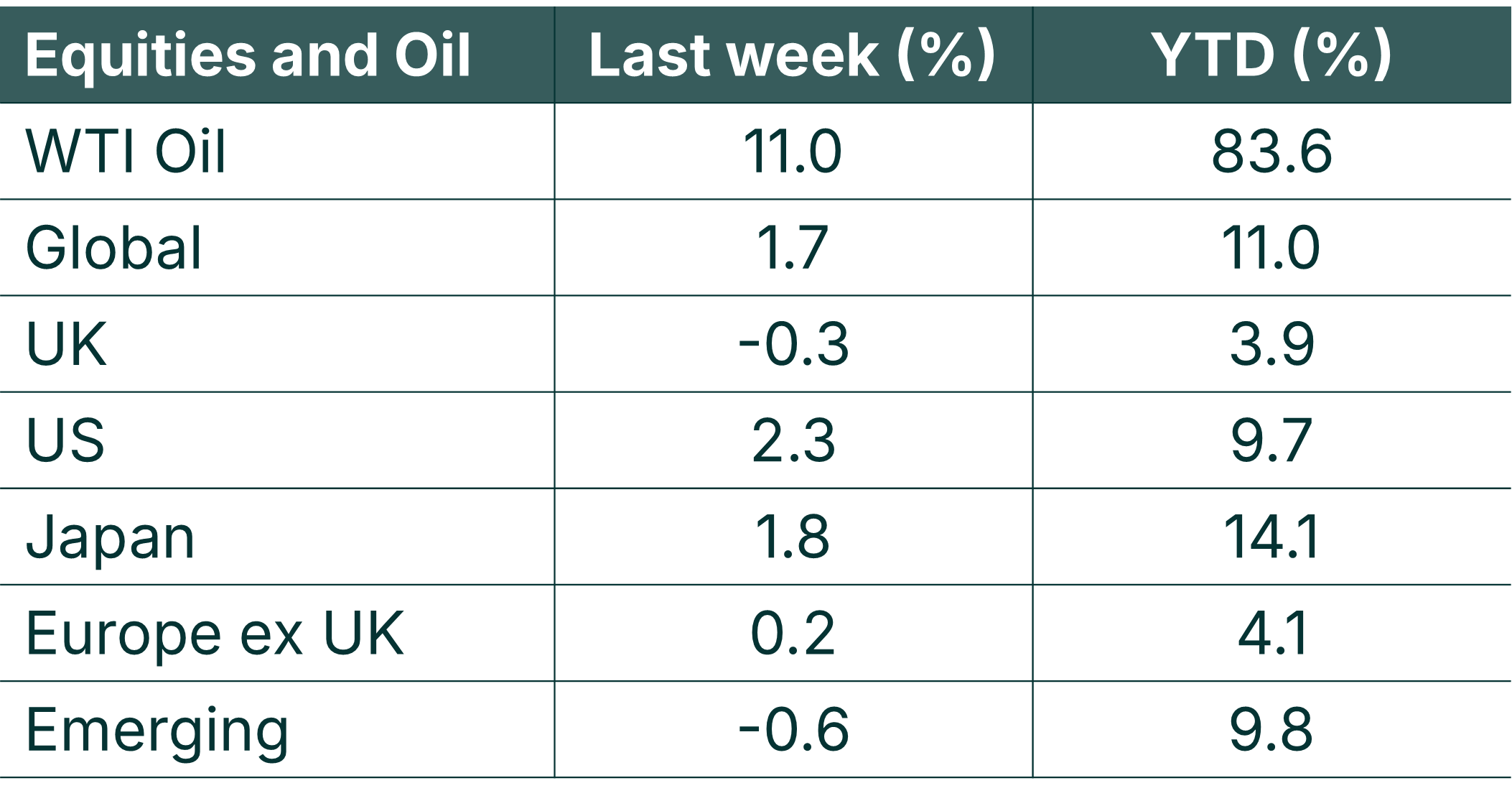

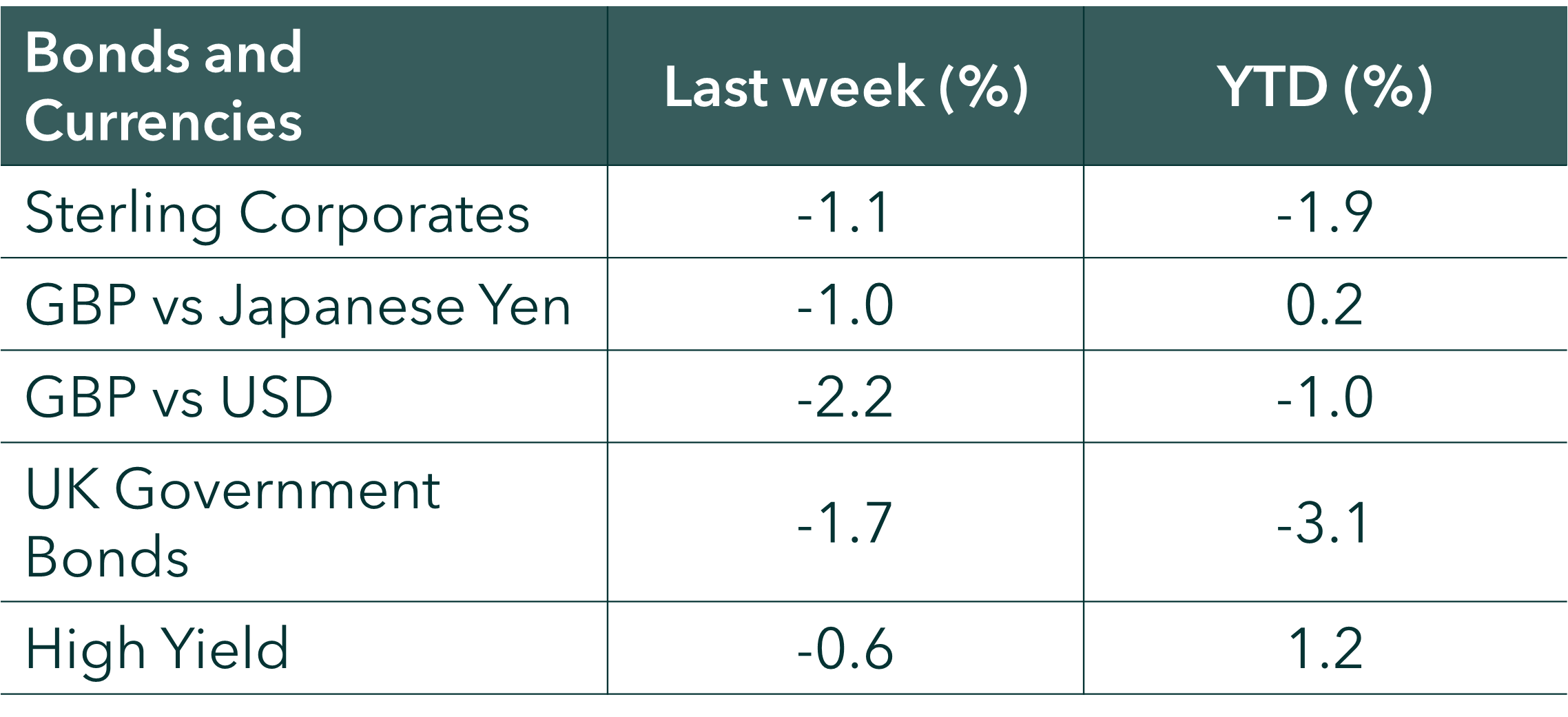

Last week

- Global equities extended gains, led by the US (+2.3%) and Japan (+1.8%), as strong earnings continued to underpin sentiment.

- UK equities were modestly weaker (-0.3%), while Europe ex-UK edged higher (+0.2%). Emerging markets pulled back (-0.6%) following a strong prior week.

- Oil was a key focus, with WTI crude rising 11% over the week amid ongoing geopolitical tensions and supply-side uncertainty.

- Corporate earnings remained broadly resilient, helping to reinforce confidence in equity markets.

- Bond markets were generally softer, with UK government bonds (-1.7%) and sterling investment grade credit (-1.1%) underperforming, while high yield proved more resilient (-0.6%).

- Economic data was mixed, with firmer US inflation offset by a stronger-than-expected UK GDP reading.

Next week

With earnings season fading, investor attention is likely to shift toward macroeconomic data and geopolitical developments.

- Corporate results will still draw attention, including results from Baidu & Ryanair (Monday), Home Depot (Tuesday), NVIDIA (Wednesday), and Walmart (Thursday).

- With fewer corporate results to drive sentiment, markets may take their lead from the broader economic and political backdrop.

- Important economic releases include UK inflation and labour market data, US Federal Reserve minutes, and Chinese retail sales and industrial production figures.

- Geopolitical developments are likely to remain in focus, particularly around the Middle East and energy markets.

Source: Bloomberg. Currency GBP.

More details

It was a busy week for Q1 corporate results, with updates from Cisco, Alibaba, Applied Materials, National Grid and Burberry. Earnings momentum remains strong, keeping global markets on track for a sixth consecutive quarter of double‑digit earnings growth, well ahead of expectations at the start of the reporting season.

On the macroeconomic front, US April CPI inflation for April, took year-on-year inflation to 2.8%. UK GDP for March surprised to the upside, lifting annual growth to 1.1%. US retail sales for April were softer but broadly in line with expectations, while German economic sentiment improved slightly but remained in negative territory.

Geopolitical developments also remained in focus. The US Treasury allowed its sanctions waiver on Russian seaborne oil to expire, a move likely to have the greatest impact on India given its position as the largest buyer. Elsewhere, developments in global health were monitored by authorities, although they remained limited in market impact.

The value of investments and the income from them can go down as well as up and you could get back less than you invested. Past performance is not a reliable indicator of future performance.

The content of this article is not intended to be or does not constitute investment research as defined by the Financial Conduct Authority. The content should also not be relied upon when making investment decisions, and at no point should the information be treated as specific advice. The article has no regard for the specific investment objectives, financial situation or needs of any specific client, person, or entity.