Oil continues to dominate the story of March markets and has opened higher in early Monday trading, following the US attack on Iran’s Kharg Island, and the ongoing effective closure of the Strait of Hormuz.

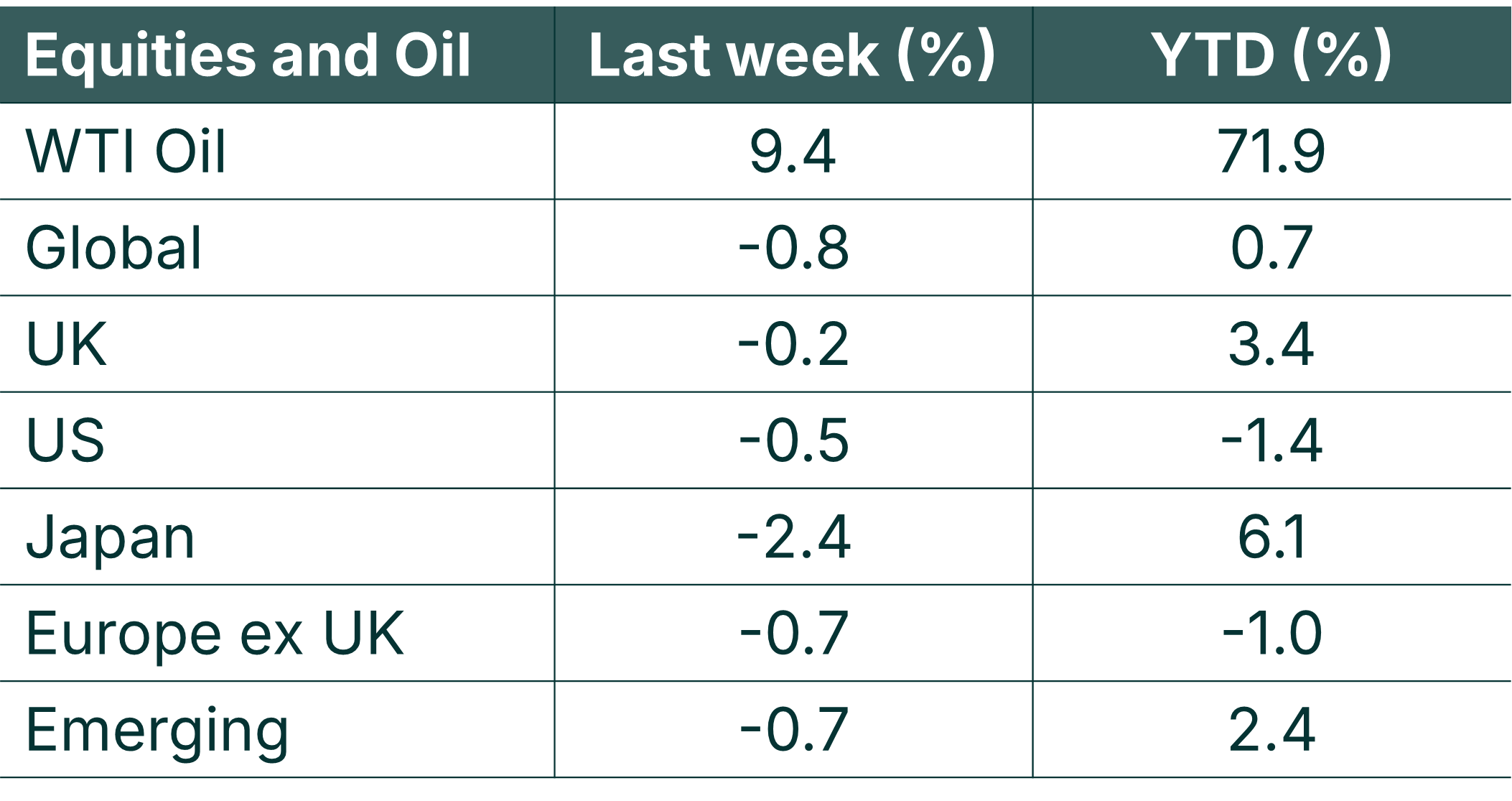

Global equity markets remained cautious but resilient, not dropping aggressively like many had speculated. Global markets were down around 0.8% over the week, with Japanese and Asian markets seeing the most impact from the Iran-US war. Japanese markets fell around 2.4% last week, but remain up year-to-date, by 6.1%.

As we saw in Magnus’ 2026 Themes piece (6 for 2026) the role of geopolitical tensions versus corporate earnings as drivers for long-term performance. They continue to closely monitor and assess the long-term impact that the current Iran-US war is having on investments.

Last week

- Looking beyond the Iran-US war, Magnus continued to see the publication of regional macroeconomic and trading data, as well as major corporate earnings, from the likes of HP, Oracle, Franco Nevada and Adobe.

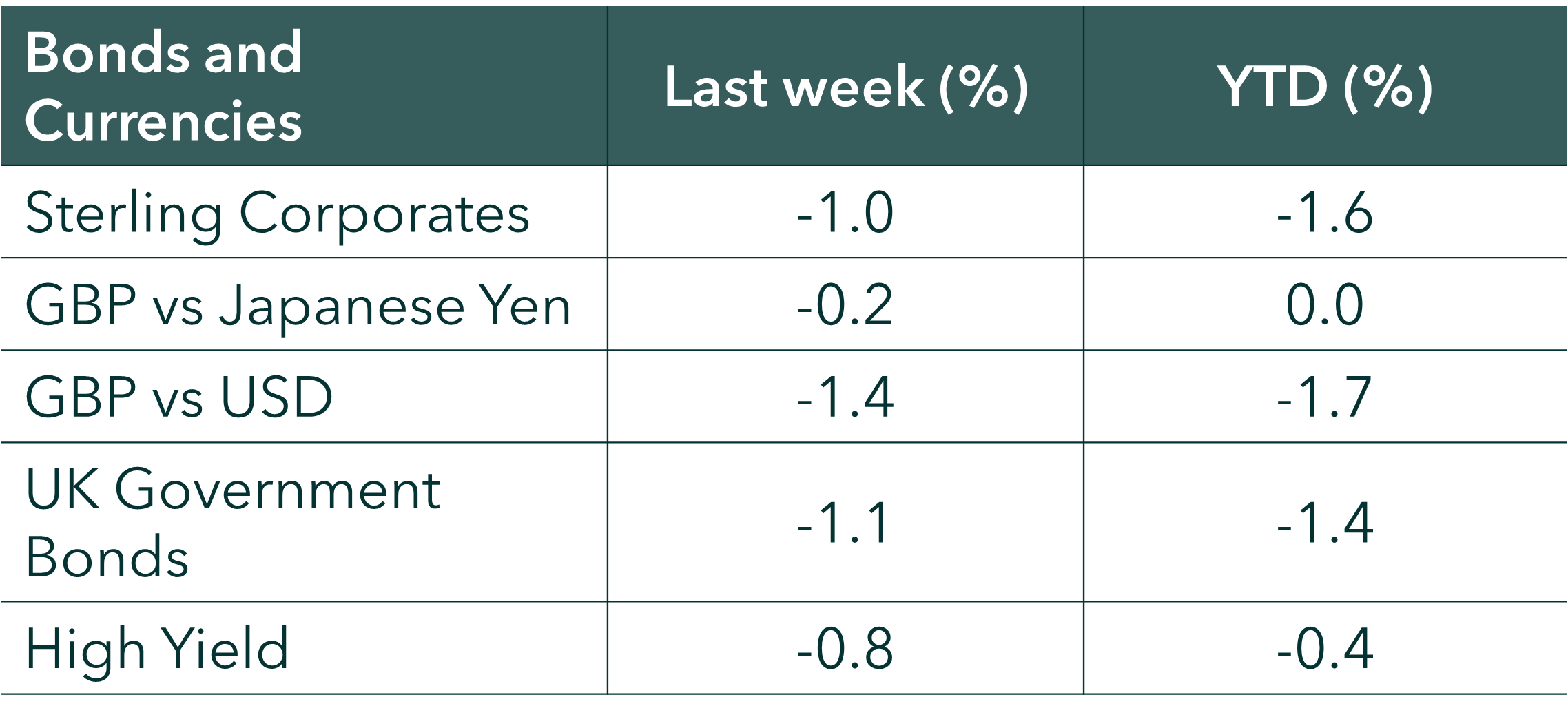

- Treasury yields continued to rise (meaning prices fell) as higher energy prices continued, prompting inflation concerns and complicating the outlook for interest rates.

- Chinese trade data showed a significant increase in both exports and imports, indicating an unexpected robustness in its economic performance.

- US inflation data for February came in line with expectation – we will need to wait until March before we begin to see the impact of the Iran-US war.

- In the UK, January GDP data was published, which came in at 0.0%, which was weaker than expected, with weaker industrial and manufacturing production.

This week

- Central banks and corporate earnings will be in focus this week.

- The Federal Reserve (US), European Central Bank, Bank of England, Bank of Japan, Bank of Canada and Reserve Bank of Australia are all set to meet to review interest rate policy.

- We will see a mix of data from major economics, including UK unemployment (Thursday), Japan’s Trade Balance, and German Economic Sentiment.

- Major business continues to release their Q4 earnings, including Accenture, Alibaba, FedEx, Lululemon and Prudential.

Source: Bloomberg. Currency GBP.

More detail on Last Week:

- A US attack on Iran’s Kharg Island had been seen by analysts as an escalation of the war with Iran, due to the island handling around 90% of Iran’s crude oil exports. US bombing was focussed on the island’s military posts, instead of the oil facilities themselves.

- From an investment perspective, as Magnus discussed in their 6 for 2026 update, corporate earnings are the key driver for equity returns, while geopolitics creates the noise. As investors, we have to look through the concerning events themselves and gauge the potential impact. For example, the slowing of trade around the world caused by the Strait of Hormuz choke point.

- Eyes will be on the US, Europe, Japan, Canadian and Australian Central Banks this week. Interest rate policy will be reviewed, with potential policy changes. US, Europe, Japan, UK, and Canadian rates are expected to be held at current levels, whereas Australian rates are expected to tick up, from 3.85% to 4.1%. Magnus anticipate a lot of attention will also be given to any commentary released, in particular the Fed Press Conference on Wednesday and the ECB Press Conference on Thursday.

- Corporate earnings remain strong and Magnus will be digging into company earnings as they are reported this week. We continue to advocate staying invested, maintaining diversification, and focusing on long‑term objectives as markets navigate the current bout of uncertainty.

The value of investments and the income from them can go down as well as up and you could get back less than you invested. Past performance is not a reliable indicator of future performance.

The content of this article is not intended to be or does not constitute investment research as defined by the Financial Conduct Authority. The content should also not be relied upon when making investment decisions, and at no point should the information be treated as specific advice. The article has no regard for the specific investment objectives, financial situation or needs of any specific client, person, or entity.