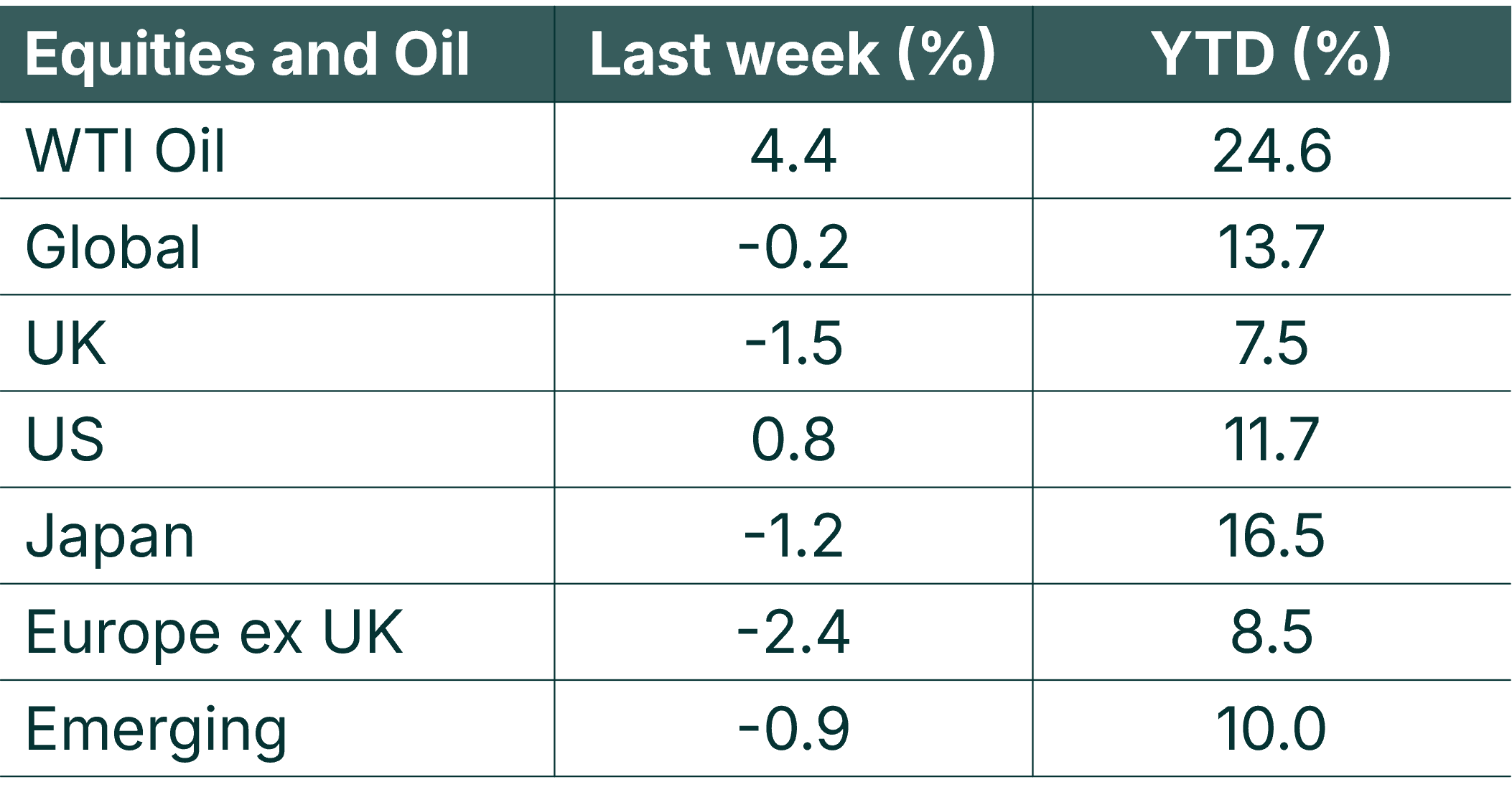

Global equity markets were little changed last week, although a stronger Pound meant that gains in overseas markets translated into modest losses for Sterling-based investors. Renewed tensions between the US and Iran pushed oil prices higher, but investors continued to favour AI-related technology companies, with the technology sector leading gains in the US and SK Hynix making a strong debut following its successful US listing.

This week, attention will remain focused on developments in the Middle East, while the US earnings season gets underway. With many of the major US banks reporting on Tuesday, investors will be looking to see whether another quarter of robust earnings can continue to support elevated equity valuations.

Last week

- Oil prices rose as tensions rose between the US and Iran.

- Global stocks posted modest losses (largely due to £ strength off-setting overseas’ gains)

- US stocks posted modest gains, with the tech and energy sectors performing well.

- UK equities fell on the week, but the UK stock market notched up 28 proposed takeovers so far this year, with both Apollo and Castlelake bidding for Easyjet.

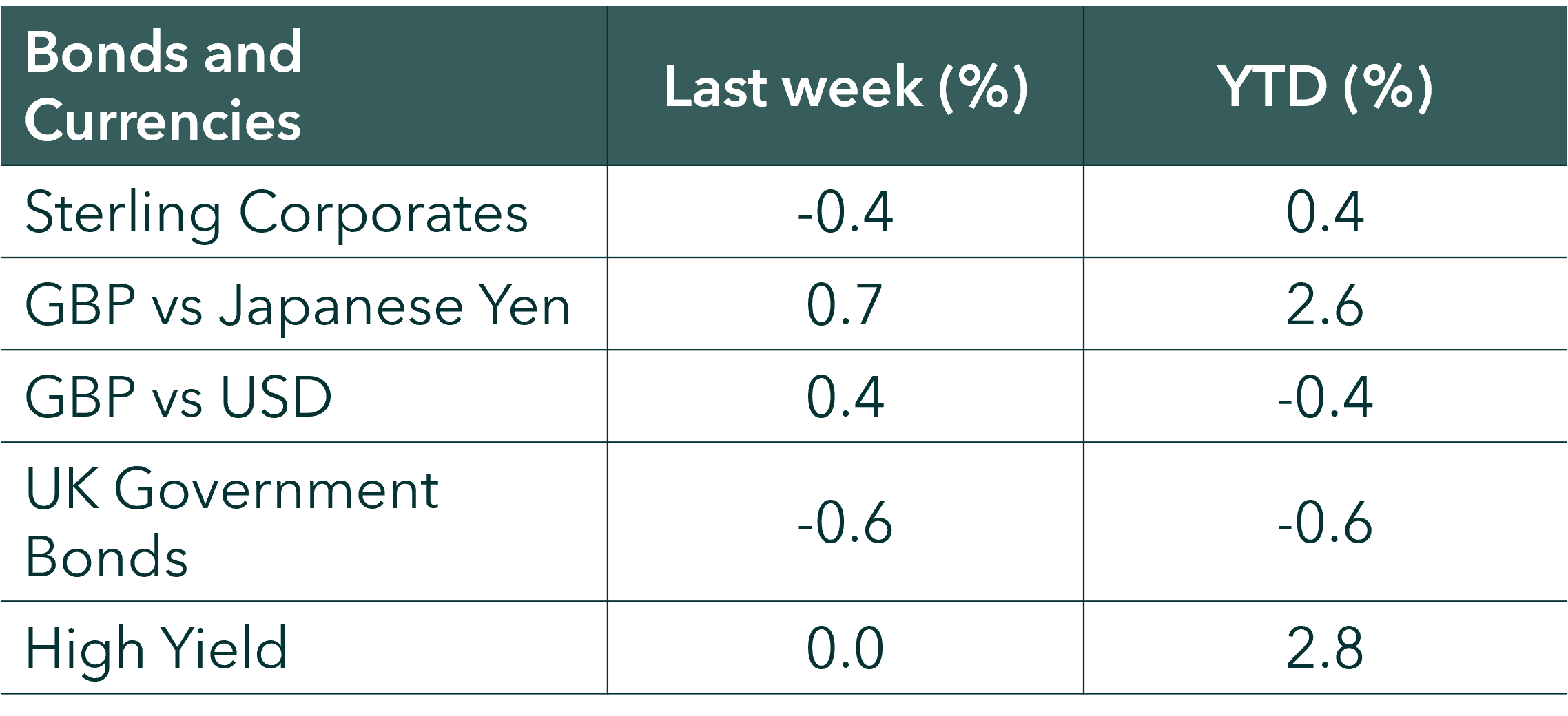

- Bond markets fell modestly.

- Andy Burnham secured party backing to be the next Labour leader.

This week

- US earnings season gets underway, with Banks such as Goldman Sachs, JP Morgan, Wells Fargo and Citigroup reporting on Tuesday. Analysts, as per Factset, are expecting YoY earnings growth of 23.6% for the US stock market : this would represent the 7th consecutive quarter of double digit earnings growth and the 2nd consecutive quarter of 20%+ earnings growth.

- US inflation is due out on Tuesday: CPI is expected to come in at 3.8% YoY (the prior print was 4.2%).

- UK growth data for May is due out on Thursday along with US retail sales.

Source: Bloomberg. Currency GBP.

More details

- Brent Crude closed the week at around $76 per barrel, following renewed tensions between the US and Iran. The oil price rose by more than 4% over the week but remains well below the $118 per barrel reached on 31 March and is only modestly above pre-conflict levels. While higher oil prices have pushed inflation expectations slightly higher, they remain far from levels that would materially alter the global economic outlook.

- Global equities declined by 2% in Sterling terms last week. The primary driver was currency rather than equity performance, with the Pound strengthening by 0.4% against the US Dollar, offsetting gains from overseas markets for UK-based investors.

- The US stock market was the best performing of the majors last week; rising by 0.8%. Gains within the US share market were driven by the technology sector (which rose by c2% and represents c40% of the entire index) and the energy sector (which rose by c3% but represents just 3% of the US share market).

- South Korean memory-chip manufacturer SK Hynix also made a successful debut on the Nasdaq. The offering was more than seven times oversubscribed, with the shares rising 13% on their first day of trading. The company is now up around 230% year-to-date, helping drive South Korea’s equity market approximately 80% higher over the same period. Despite this exceptional performance, SK Hynix still trades on around five times forward earnings, reflecting expectations that current earnings may prove cyclical even as demand for AI-related memory chips remains exceptionally strong.

- UK equities fell by around 5% over the week. Gains in the energy sector were more than offset by an 11% decline in AstraZeneca, following disappointing Phase III clinical trial results.

- Takeover activity in the UK continued at pace. EasyJet became the latest UK-listed company to attract acquisition interest, with Apollo making a £5.7 billion approach, exceeding an earlier proposal from Castlelake made only days before. According to Peel Hunt, 28 takeover bids have now been announced for UK-listed companies this year, with a combined value of £59.7 billion—around 27 times the value of companies that have listed on the London market during the first half of 2026. The continued level of takeover activity reinforces our view that many UK-listed companies continue to trade at attractive valuations relative to international peers.

- Bond yields rose last week, which meant that bond prices fell. UK Government bonds fell in value by about 6%, whilst US Treasuries fell by about 0.4%. Rising inflation expectations were the key driver of the sell-off in bonds, with expected inflation rising on the back of the rise in the Oil price.

- On Thursday, 322 of Labour’s 403 MPs backed Andy Burnham to succeed Keir Starmer as Labour leader, paving the way for his formal appointment on 17 July.

The value of investments and the income from them can go down as well as up and you could get back less than you invested. Past performance is not a reliable indicator of future performance.

The content of this article is not intended to be or does not constitute investment research as defined by the Financial Conduct Authority. The content should also not be relied upon when making investment decisions, and at no point should the information be treated as specific advice. The article has no regard for the specific investment objectives, financial situation or needs of any specific client, person, or entity.