The announcement of a US–Iran ceasefire prompted a decline in oil prices and a rally in risk assets. However, the Strait of Hormuz remains effectively closed, the ceasefire is fragile and much now hinges on upcoming negotiations.

Peace talks between the US and Iran in Islamabad over the weekend have ended without agreement, so we will continue to closely monitor the situation in the Middle East. Until there is a clear resolution, economic disruption and inflation risks remain, keeping central banks on alert.

Source: Bloomberg. Currency GBP.

Last week

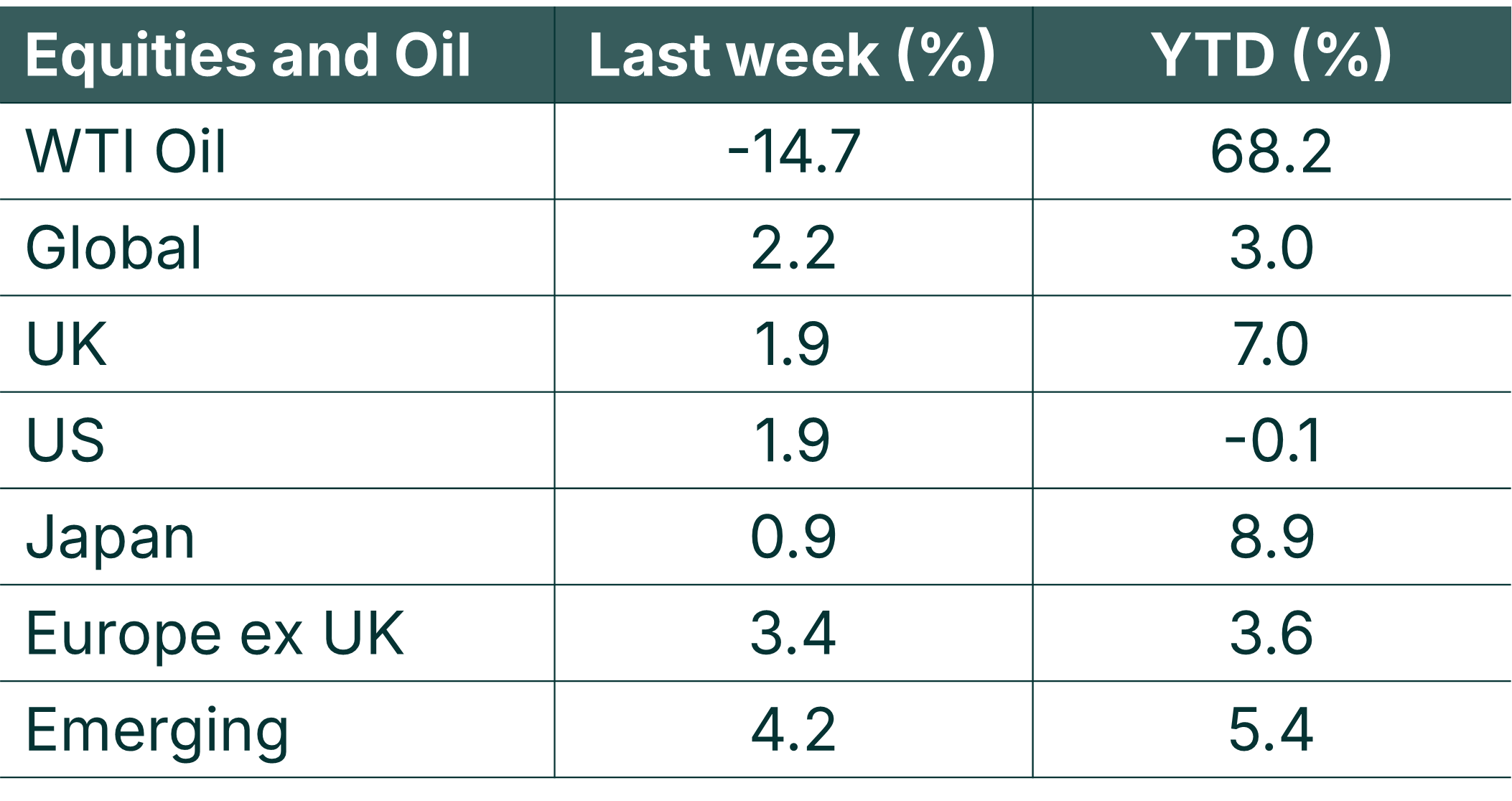

Investment markets posted good gains last week, with both bonds and equities rallying on hopes of a de-escalation to the Iran conflict.

- United States: Although the temporary ceasefire helped steady markets, the conflict’s effects were visible in March CPI data, consumer sentiment, and near term inflation expectations.

- United Kingdom: Tighter financial conditions and slightly weaker final PMI readings underscore the ongoing headwinds to the UK economic outlook until there is a firm peace deal in the Middle East. However, the UK index gained 1.9% last week, driven by a relief rally as oil prices eased and in particular from strong gains in the mining and banking sectors.

- Japan: Japanese equities gained 0.9% last week in sterling terms. Prime Minister Sanae Takaichi announced that Japan will release additional state oil reserves starting next month, extending measures taken since March to draw on national and private stockpiles to cushion the domestic economy from oil driven price pressures.

- China and Hong Kong: a short week for these markets due to holidays. China’s President Xi Jinping received Taiwan’s main opposition party leader on Friday, in a rare meeting, which saw both sides stress a desire for cross-strait peace.

This week

- US Q1 earnings season begins: Key reports expected from major banks including JPMorgan Chase, Wells Fargo, Citigroup, Bank of America, Morgan Stanley, and Goldman Sachs.

- Tech & Industrials: Netflix, ASML, and semiconductor names are in focus for Q1 earnings releases.

- Geopolitics: Monitoring the US-Iran ceasefire negotiations.

- UK GDP data is due on Thursday, also Tesco annual earnings and Imperial Brands, Antofagasta and Barratt Redrow trading statements are expected.

More detail

- US stocks climbed 1.9% over the week in Sterling terms, extending the prior week’s gains. Easing Middle East tensions pushed WTI oil prices down roughly 15%, helping fuel the rally.

- Rising energy costs drove the March US CPI print to 3.3% year over year, well above the Federal Reserve’s 2% long run target and sharply higher than February’s 2.4% reading. The energy component of the index surged 12.5% from a year earlier. The near term trajectory will also be determined by oil price moves.

- Revised data reveals US economic growth slowed considerably at the end of 2025. Data released last week showed Q4 GDP expanding at a 0.5% annualized rate, down from the mid March estimate of 0.7% and February’s initial 1.4%. The downward revision primarily reflected weaker than expected investment. By contrast, Q3 2025 growth reached 4.4%, a two year high.

- Ahead of US banks kicking off earnings season, Wall Street analysts trimmed expectations slightly. As of Friday, consensus forecasts from FactSet published online projected S&P 500 earnings growth of around 12.6% for Q1, down from 13.2% the week before. However, either outcome would still mark a sixth straight quarter of double digit growth.

The value of investments and the income from them can go down as well as up and you could get back less than you invested. Past performance is not a reliable indicator of future performance.

The content of this article is not intended to be or does not constitute investment research as defined by the Financial Conduct Authority. The content should also not be relied upon when making investment decisions, and at no point should the information be treated as specific advice. The article has no regard for the specific investment objectives, financial situation or needs of any specific client, person, or entity.