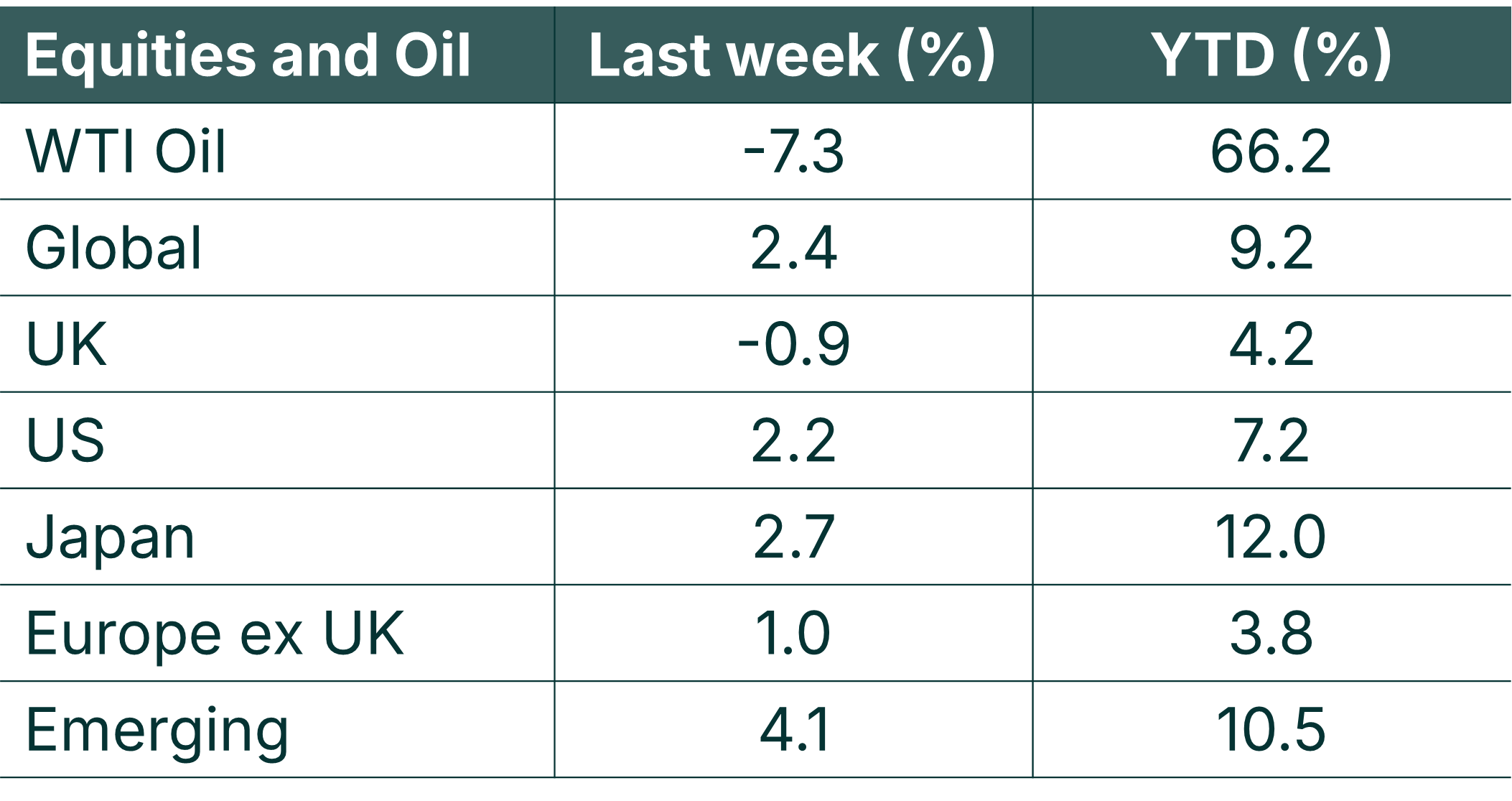

Last week was another positive one for Global Equity markets which are now up over 11% from their lows on 27th March 2026. Strong earnings from the technology sector continued to drive gains.

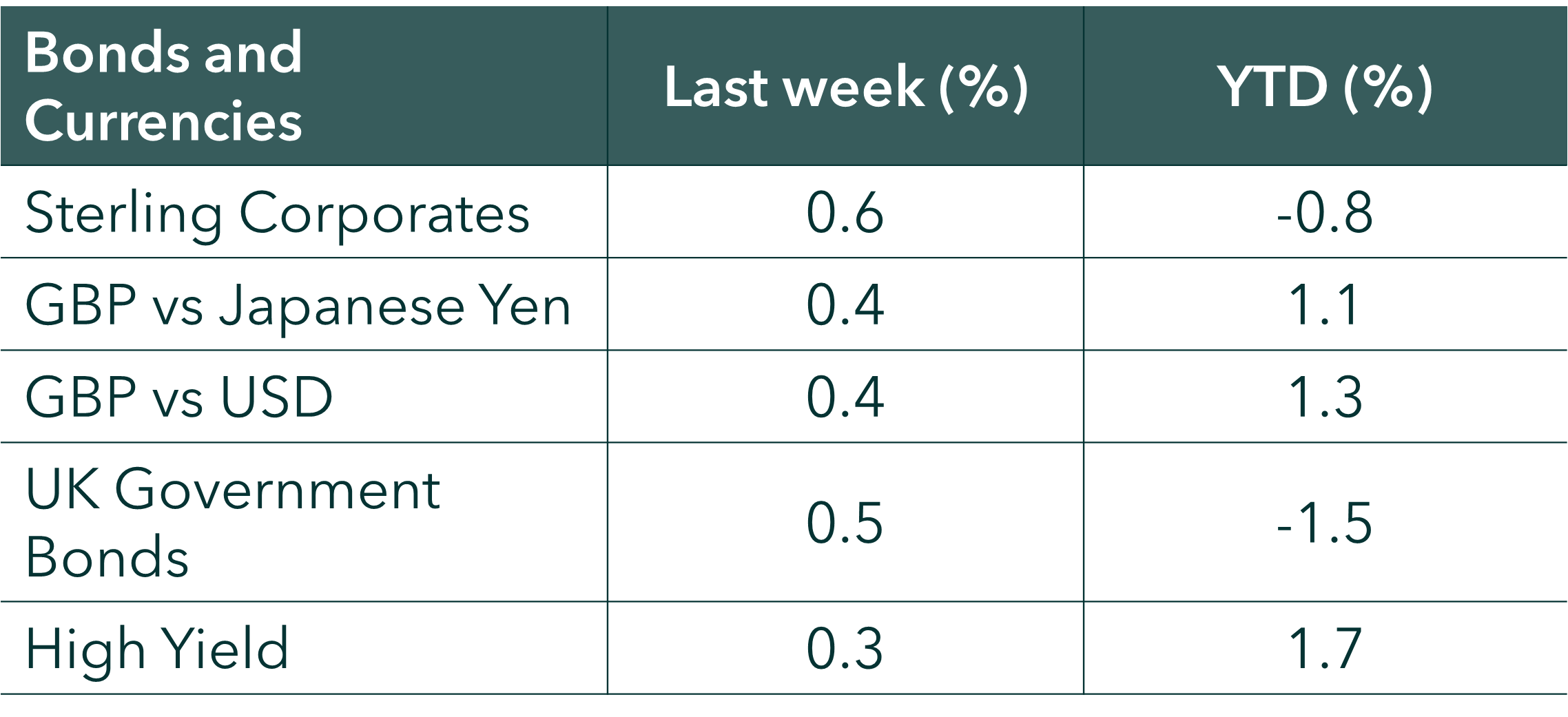

Bond markets also posted modest gains last week, with both sovereign yields and credit spreads rallying.

This week is a quiet one in terms of scheduled data, with US inflation (out on Tuesday) likely the focal point for markets.

Source: Bloomberg. Currency GBP.

Last week

- Global stock markets posted decent gains, with the technology sector continuing to drive returns

- US Corporate earnings continued to come in strong

- UK shares gave back some ground, with the energy sector weighing

- Bond markets posted modest gains

- US jobs data came in better than expected

Next week

- It’s a relatively quiet week on the economic and corporate data front

- Tuesday sees the release of US inflation data, whilst Thursday sees the release of US retail sales data

- UK economic growth data is released on Thursday

- It is quite light on the corporate earnings front, but we do have results from the likes of Cisco (Weds) and National Grid and Burberry on Thursday.

More details

Global stock markets rose by 2.4% last week, with the technology sector continuing to drive gains. The Global Technology sector was up over 7% last week and accounts for just shy of 30% of the weight within the global share market.

US Corporate earnings continued to be very strong last week. We are now 89% of the way through the US earnings season and the blended growth rate for the US S&P 500 is 27.7% (as per Factset data). This puts us on track for the 6th consecutive quarter of double digits earnings growth and is significantly higher than the anticipated (at end March 2026) growth rate of 13.1%.

US technology (with its c35% index weight) has been the key driver of US earnings’ growth and it has delivered a growth rate of c50% YoY. There have, however, been strong gains from other sectors, with Financials, Industrials and Utilities all strongly surprising to the upside and delivering YoY growth of over 17%.

UK shares fell back by about 0.9% last week, with much of this pull-back being driven by the energy and utilities sector, which gave back some of their recent gains. The energy sector (c11% of the UK share index) was hardest hit, falling by c6% on a declining oil price.

Bond markets rose modestly last week, with UK Government bonds up by 0.5% on the week and UK corporate bonds up by 0.6%. Credit spreads (both for investment grade and high yield) are back to trading at historically tight levels. UK 10-year Government bond yields closed out the week yielding 4.9%: slightly lower on the week but still trading around levels not seen since summer 2008.

US jobs data came in better than expected, although the strength was somewhat flattered by a decline in the % of people working or seeking work, with this measure (the “participation rate”) falling to its lowest level since October 2021. For the month of April, the US economy added 115k jobs (much more than the 65k that had been expected by economists surveyed by Bloomberg), whilst the unemployment rate held steady at 4.3%. Payroll growth for the previous month was revised upwards, and this made for the strongest 2-month period of nonfarm payroll increases since 2024.

The value of investments and the income from them can go down as well as up and you could get back less than you invested. Past performance is not a reliable indicator of future performance.

The content of this article is not intended to be or does not constitute investment research as defined by the Financial Conduct Authority. The content should also not be relied upon when making investment decisions, and at no point should the information be treated as specific advice. The article has no regard for the specific investment objectives, financial situation or needs of any specific client, person, or entity.