The Chancellor, Rachel Reeves, delayed her Autumn 2025 Budget until 26 November, creating a second consecutive protracted period of pre-Budget speculation. The late timing also meant that her Spring 2026 Forecast has arrived just under fourteen weeks after her previous parliamentary set piece.

It has, however, been an eventful few months, with U-turns on both the 2024 Budget measures relating to inheritance tax (IHT) agricultural and business reliefs and the 2025 Budget proposals for business rates. And that is before the political storms of the winter are considered, which have had their own economic impact via the uncertainty created.

The current flare up of hostilities in the Middle East may, as the Office for Budget Responsibility notes, have “very significant impacts on the global and UK economies”. In turn that could call into question the Forecast numbers. With oil prices already affected and the stock and bond markets reacting negatively to the uncertainty created, the Chancellor will be hoping the repercussions do not prove too serious for UK plc by the time of her next Budget this autumn.

Will we be moving to one fiscal event a year?

Like some of her predecessors, Rachel Reeves has regularly claimed to want only one major fiscal event each year. In the Autumn 2025 Budget Red Book, she spoke of “strengthening the fiscal framework to deliver on the government’s commitment to hold one major fiscal event (Budget) per year, supporting the economy with greater policy certainty”. The Finance Bill, now on its way through parliament, contains the necessary amending legislation. It requires the Office for Budget Responsibility (OBR) to produce only one assessment of the fiscal headroom each year, rather than two, as it has previously.

Nevertheless, twice a year the OBR must still undertake and publish the data used to calculate the headroom figure – hence the Spring Forecast (not this time a Statement). What the watchdog will not do is make a fiscal mandate assessment, although many external forecasters will step in to do so.

It is easy to see why Rachel Reeves would not now want a full OBR assessment, given the problems she faced last year. Back then, disappointing preliminary projections prompted the announcement of hastily designed benefit reforms to make the numbers balance, only for a subsequent summer U-turn to quell a back bench rebellion. With no official OBR assessment in March 2026, there is less pressure for any fiscal action. That helps after the two post-Budget revenue-reducing U-turns on IHT) reliefs and business rates.

From a longer term, strategic viewpoint, avoiding an annual cycle of Budget and quasi-Budgets makes sense, especially when, as now, the gap between events is only a few months. Many countries manage with only one yearly budget, resorting only to supplementary budgets when serious problems arise. Ironically, in the UK that might need to happen soon, depending upon developments in the Middle East.

The Economic Background to the Spring Statement 2026

Rachel Reeves delayed her Autumn 2025 Budget until 26 November, creating a second consecutive protracted period of pre-Budget speculation. The late timing also meant that her Spring Forecast has arrived just under fourteen weeks after her previous parliamentary set piece.

It has, however, been an eventful few months, with U-turns on both the 2024 Budget measures relating to IHT agricultural and business IHT reliefs and the 2025 Budget proposals for business rates. And that is before the political storms of the winter are considered, which have had their own economic impact via the uncertainty created.

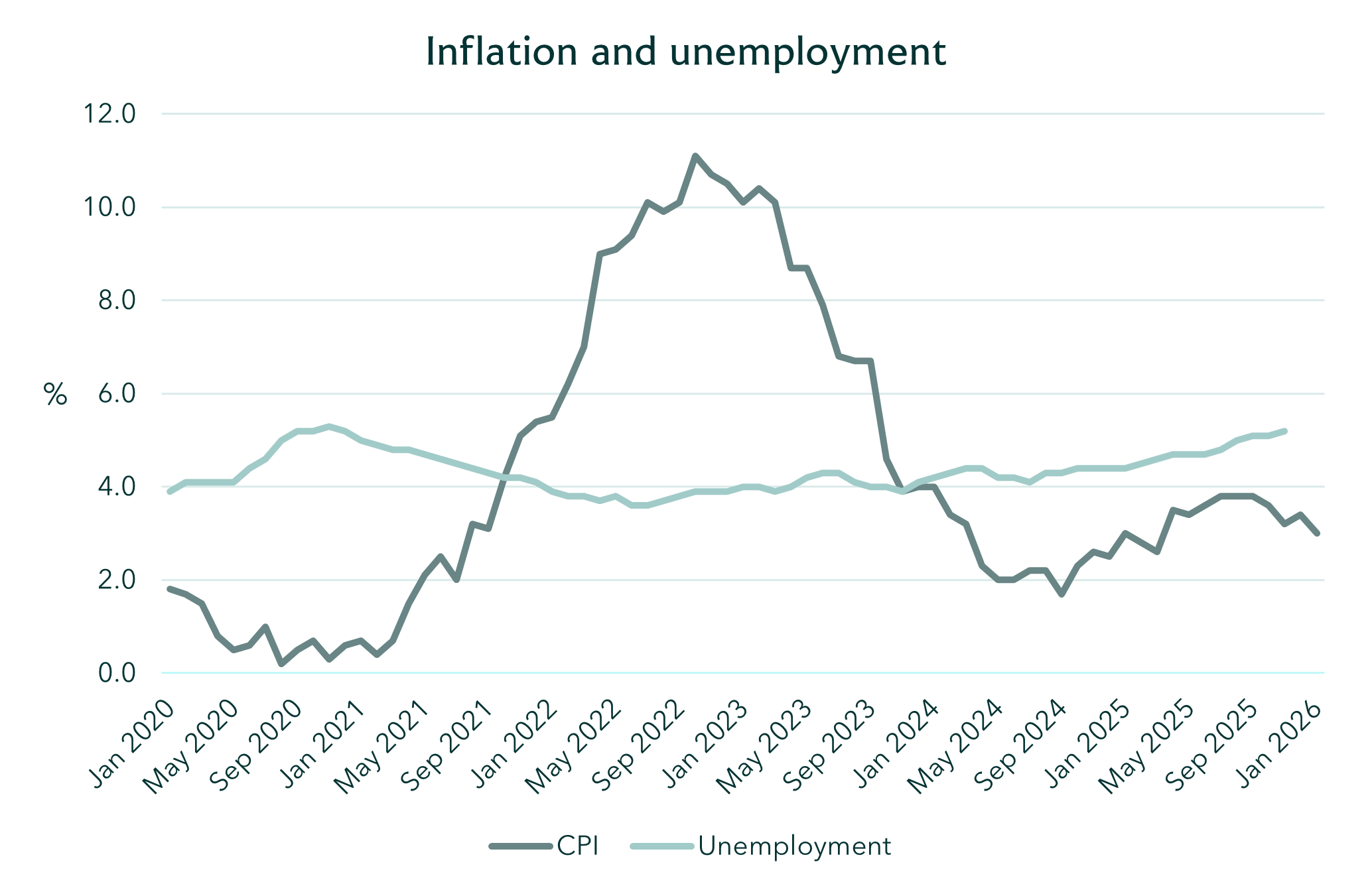

The Autumn 2025 Budget took place against a backdrop of UK GDP growth having slowed to just 0.1% in the third quarter, after starting the year with a first quarter reading of 0.7%. Preliminary figures from the Office for National Statistics (ONS) released in mid-February 2026, suggested GDP growth remained at 0.1% in the final quarter and that 2025 GDP growth was 1.3%. In the same month, the ONS also published its usual monthly data on the labour market, inflation and retail sales:

- Unemployment for October to December 2025 was 5.2%, up from 4.4% for the corresponding period a year ago and above pre-coronavirus pandemic rates. The hardest hit were those aged 16 to 24, where the unemployment rate was 16.1%, the highest for over a decade.

- Average weekly earnings annual growth (with and without bonuses) was 4.2%, down from 5.9% for October to December 2024. However, the latest figure is distorted by the bunching of public sector pay settlements – the private sector earnings growth (with and without bonuses) was 3.5%.

- Annual CPI inflation was 3.0% in January 2026, unchanged from a year ago. The Bank of England, along with many independent forecasters, anticipate that inflation will be close to the Bank’s 2.0% by April.

- The volume of retail sales rose by 0.1% in the three months to January 2026, compared with the previous three months. However, January alone saw a 1.8% rise with the ONS noting there was “a good start to the year for non-food stores”. This came on top of a 0.4% rise in December and a 0.4% November drop – probably attributable to that late Budget.

Source: Office for National Statistics

Spring Forecast 2026

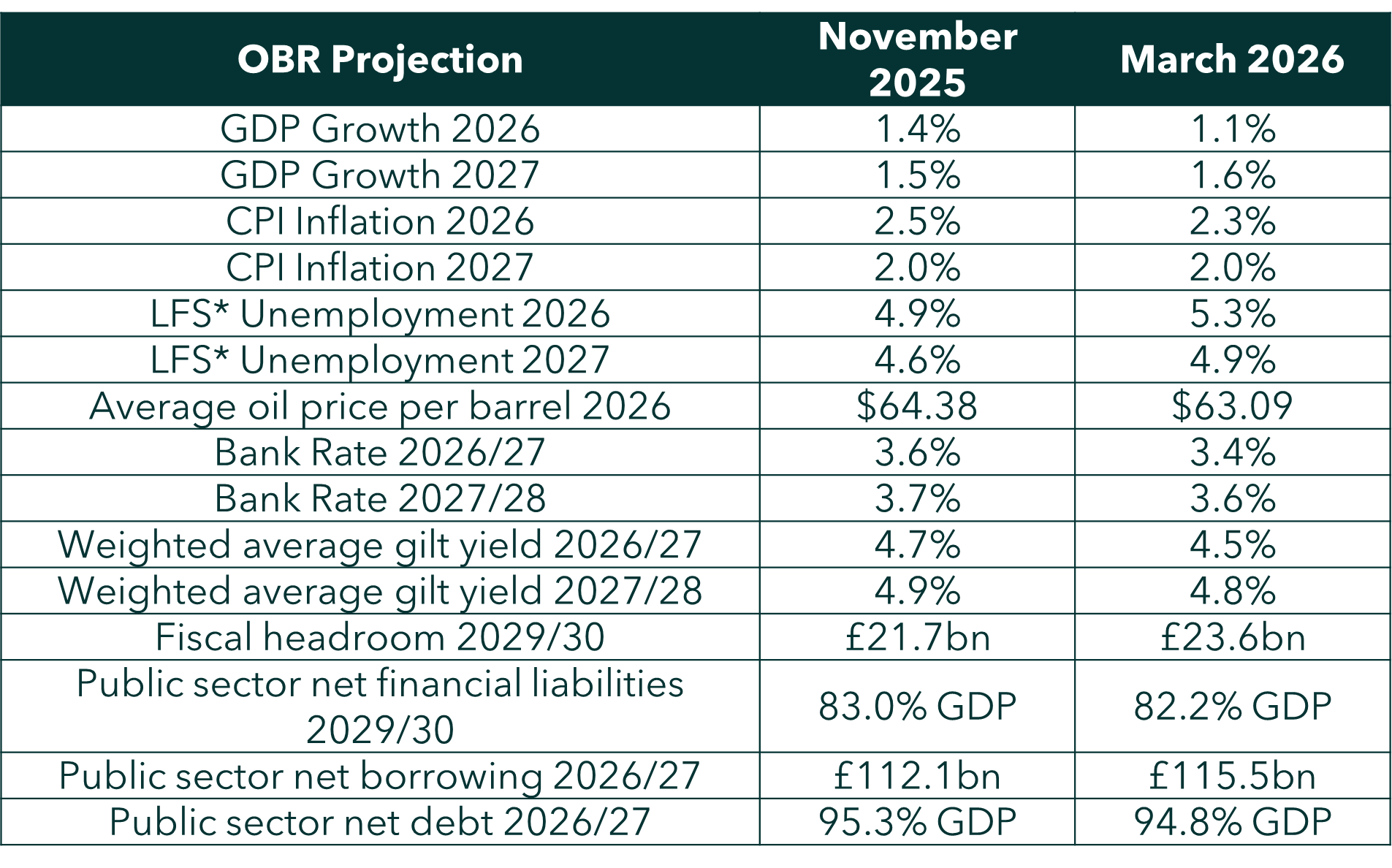

OBR projections Autumn Budget 2025 vs Spring Forecast 2026

*Labour Force Survey

Source: Office for Budget Responsibility

With little more than three months since the OBR published (slightly prematurely…) its last Economic and Fiscal Outlook (EFO), it was likely there would be few significant changes in the numbers.

-

Growth

As the table above shows, the OBR’S projection for economic growth in the current year has been cut to 1.1%, bringing it into line with the February market consensus, but still above last month’s Bank of England’s forecast of 0.9%. The OBR increased its projections for growth in both 2027 and 2028 to 1.6% (from 1.5%), largely countering the impact of its 2026 reduction over its five-year forecast period.

-

Inflation

The OBR’s inflation projection for this year was cut by 0.2% to 2.3%, which closely matches the Bank of England’s own estimate for inflation. To a degree this fall of inflation has been engineered by the government with the actions it has taken on administered prices, such as the energy price cap and rail fares.

-

Unemployment

The better outlook for inflation may also be due in part to a gloomier projection for unemployment, which the OBR now sees as averaging 5.3% in 2026, against the 4.9% which it projected back in November 2025. Unemployment stays above those previous EFO levels until 2029, by which time it is projected to have fallen back down to 4.2%, marginally below where it was in 2024.

-

Fiscal headroom

Fiscal headroom, which caused so much angst for the Chancellor a year ago, barely received a mention in her speech. The ‘stability rule’ headroom – the extent to which the current budget is projected to be in surplus by 2029/30 – rose from £21.7 billion to £23.6 billion. The increase was the result of a mix of factors, including:

- Revisions to the OBR’s assumptions, such as on interest rates.

- Buoyant tax receipts, visible in the record £30.4 billion January surplus recently reported by the Treasury.

- Increased spending on special educational needs and disabilities (SEND), averaging £4.2 billion a year between 2028/29 and 2030/31.

- Other increased spending, such as the cost of rejoining the Erasmus programme.

- The costs of U-turns on IHT reliefs and business rates for pubs and live music venues. For all the attention these received, the loss of revenue is estimated to be an average £0.1 billion a year for each.

-

Borrowing

Government borrowing for the current year is now projected to be £132.7 billion, down £5.5 billion from the OBR’s November 2025 number, but £15 billion more than it projected a year ago. 2026/27’s borrowing is projected to be £115.5 billion, 3.1% higher than projected in November. Thereafter borrowing is below November’s projections.

-

Gilts

The uptick in borrowing contrasts with a £51.6 billion drop in projected gilt sales to £252.1 billion in 2026/27. Over half that decline stems from £27.5 billion less in gilt redemptions requiring refinancing in the next financial year. Net debt interest in 2026/27 is projected to be £109.4 billion, £3.9 billion below the November forecast, thanks to lower inflation and interest rates.