The potential impact

Using a simple case study, Dan illustrated how these changes could affect a typical financial planning client that has been building wealth in their pension fund under the current rules for succession planning.

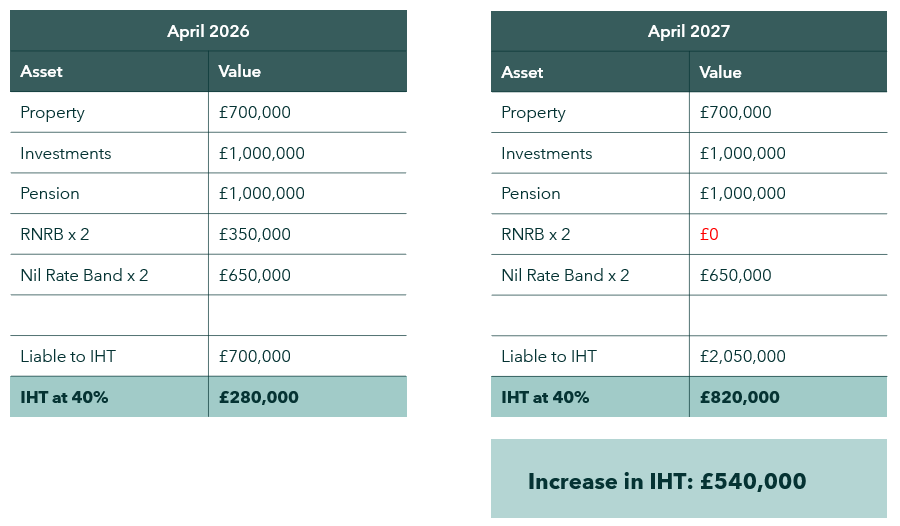

In the example shown, an estate that may currently result in an inheritance tax liability of £280,000 could increase to £820,000 after 6 April 2027, under the new rules – a difference of £540,000. This is because the value of the estate is now above £2m, triggering the reduction of the Residence Nil Rate Band (RNRB), which is £1 reduced for ever £2 over £2m).

While this is purely illustrative, it highlights how important it is to review planning sooner rather than later.

The £2 million Residence Nil Rate Band (RNRB) Cliff Edge

For illustrative purposes only. Based on our current understanding of UK pension legislation law, tax law and HM Revenue and Customs’ practice April 2026.

Inheritance Tax Planning opportunities

There are a range of established strategies that can help manage and mitigate IHT exposure. These may include:

- Gifting or spending during lifetime

- Using trusts as part of estate planning

- Considering Business Relief investments

- Reviewing income options such as annuities

- Putting appropriate protection in place

An important theme from the session was the need to balance planning for the future with maintaining control and flexibility in the present. Many of the strategies discussed can help reduce the value of an estate for tax purposes, while still supporting income needs and access to capital during your lifetime.

Regular reviews are also key. As legislation evolves and personal circumstances change, ensuring that arrangements remain aligned to your long-term objectives can help avoid unintended consequences and provide greater confidence over time.

A joined-up approach

Alongside Dan’s session, we were joined by our partners:

Together, this reinforced the value of a coordinated approach, bringing together financial planning, legal expertise, and protection to support long-term outcomes, all coordinated by Wren Sterling Financial Planners.