Over the weekend, Iranian state media and multiple international news organisations confirmed the death of Iran’s Supreme Leader, Ayatollah Ali Khamenei, following large‑scale U.S. and Israeli military strikes on targets in Iran.

This development marks a profound escalation in an already volatile regional conflict, with significant and deeply concerning humanitarian and geopolitical implications.

Our thoughts are with all civilians affected by these events, and with any of you who have friends, family or business connections in the region. We remain acutely aware that behind the headlines are human lives, communities and families facing uncertainty and loss.

Market reaction to date

Financial markets have responded, at least in the early stages, by pricing in heightened uncertainty rather than clear signs of sustained economic disruption. So far we have seen:

- A significant rise in oil prices

- Modest declines in major equity indices

- Flows into perceived safe‑haven assets such as the U.S. dollar

These reactions reflect concerns about regional stability, rather than any expectation of economic gain.

In this note, we set out the background to the escalation, the key investment implications, what history suggests and how the team at Magnus are positioning client portfolios.

Implications for Energy markets

Energy markets are understandably the primary focus. Iran is a meaningful exporter of crude oil, and the Strait of Hormuz remains one of the most critical chokepoints in global energy supply, with a substantial share of global oil shipments passing through it. The potential for disruption to shipping through this narrow corridor is a key driver of the recent volatility in oil prices.

OPEC+ has indicated a willingness to increase output to help stabilise supply. While Brent crude prices have risen sharply, they remain below previous historical peaks.

Two broad scenarios remain possible:

- Normalisation – If shipping routes and energy flows stabilise, market volatility may prove temporary.

- Persistent Disruption – If the region experiences prolonged instability, higher energy prices could feed through into inflation, affect central bank policy, and place pressure on global growth.

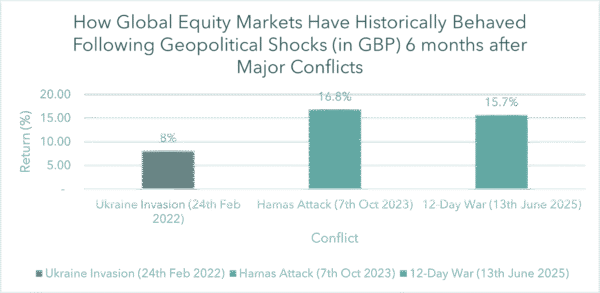

What History Suggests

While every conflict is unique and this one carries exceptional humanitarian and geopolitical risks, financial markets have historically distinguished between short‑term geopolitical shocks and longer‑term economic fundamentals. Over time, corporate earnings, valuations and economic conditions tend to exert a greater influence on investment returns than short‑term geopolitical events.

While periods of market turbulence can be unsettling, emotional, short‑term reactions have rarely served long‑term investors well.

The chart below illustrates how global equity markets have performed six months after prior recent major geopolitical events. (Source: Bloomberg / MSCI world total return in GBP.)

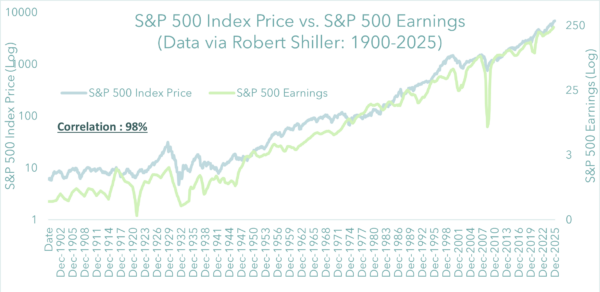

Long-term equity returns are driven primarily by corporate earnings. The US has just completed its fifth consecutive quarter of double-digit earnings growth, and there is currently no evidence that this conflict has materially altered the global earnings outlook.

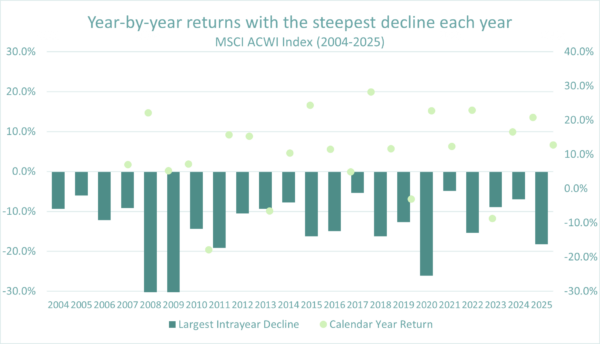

“Choppiness”, or “volatility” as we call it, is all part of the parcel of investing in equity markets. We’d note that over the last 20 years, equity markets have averaged a return of 10% but have had an average intra-year decline of 14.4%.

Periods of market stress are uncomfortable, but reacting emotionally has rarely proved beneficial for long-term investors.

How Magnus has positioned portfolios

For clients invested within Magnus, our sister fund management business, its positioning over the past 18 months has been guided by diversification, valuation discipline and prudent risk management, rather than by attempts to anticipate specific geopolitical crises. Actions include:

- Increasing allocations to UK equities to reduce dependence on concentrated markets

- Broadening U.S. equity exposure to reduce sector concentration risk

- Maintaining meaningful U.S. dollar exposure

- Holding short‑dated bonds to provide stability and flexibility

These steps have been designed to support resilience across a wide range of possible outcomes.

Conclusion

We do not in any way wish to minimise the severity of the current situation or the profound human impact it carries. From an investment perspective, while the situation remains highly fluid, current evidence suggests that markets are experiencing a volatility shock, not yet a fundamental or systemic economic break.

Our approach remains steady: disciplined asset allocation, valuation awareness and careful risk management. We will continue to monitor developments closely and will adjust positioning only if the underlying economic outlook changes materially.

In the meantime, history suggests that a measured, diversified and long‑term perspective remains the most effective approach for investors, particularly during periods of uncertainty.

IMPORTANT

The value of investments can fall as well as rise. You may get back less than you invest.

Past performance is not a guide to future returns.