A small pay rise leaves parents worse off

Families with young children face another complication and punch to the stomach.

Once an income exceeds £100,000, eligibility for tax-free childcare and certain funded childcare hours stops. That loss can add several thousand pounds of cost each year, with the combined effect pushing the real marginal rate far higher than 60 per cent ‘tax trap’.

This creates a strange outcome. A small pay rise can sometimes leave a household much worse off.

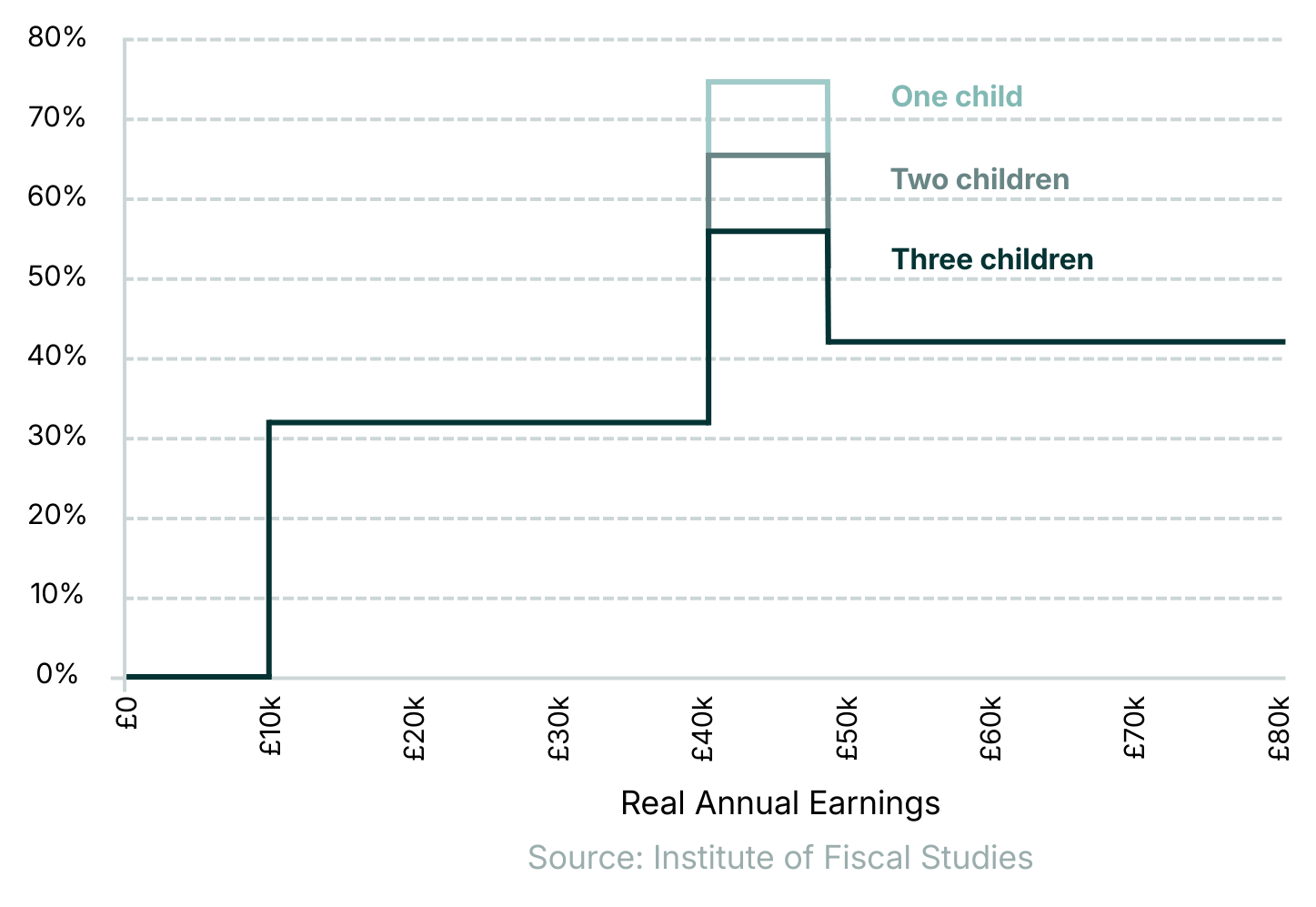

Note: Marginal tax rate for a single earner, or the higher earner in a couple, excluding all benefits other than child benefit. Employer NICs and the 2022 National Insurance rise (to be reversed) are also excluded. Source: Institute for Fiscal Studies.

Why this matters more than it used to

The median salary in the UK in April 2025, the latest figures we have, was £39,039That is not a small number of people. The £100,000 threshold has been frozen since 2010. Salaries have not, even if the long-term trend of wage rises has somewhat stagnated post the Global Financial Crisis of 2008. As incomes rise, more people find themselves in this income band. Senior teachers, NHS consultants and nurses, and lawyers now reach this level in mid-career rather than at the end of it.

Introduced in 2010 by then Labour Chancellor Alistair Darling, it has been kept by successive Chancellors of both hues for one very clear reason – the majority don’t notice it. Stealth taxes, or fiscal drag in economic parlance, are one of the easiest ways to make a Budget balance (did someone say ‘headroom’?). Instead, more people are being pulled into the trap each year.

Even MPs Are Getting Close

But I wonder if this could become the next “hot topic” of UK political debate. We will have all seen in recent weeks and months the debate around Plan 2 Student Loans and the arguably excessive level of interest that is charged on these “loans”, coupled with the political fallout as Martin Lewis makes it the current “cause célèbre”.

Why this could have captured the imagination of a number of recently elected MPs who may be caught in the net of these Plan 2 loans is anyone’s guess.

On a completely unrelated note, it was confirmed this week by the Independent Parliamentary Standards Authority (IPSA) that the basic salary of an MP would be rising by 5% to £98,599 from April 2026. With an aim to move towards a salary of around £110,000 by the end of the Parliament, due in 2029. That puts the salary of an MP dangerously close to the £100,000 threshold where Personal Allowance starts to get clawed back. A salary increase of only around 1.5% next year would push them above £100,000. Yes, some MPs have second (or indeed third, fourth, and fifth) incomes which already push them above the £100,000 threshold. But many do not, and so would not have been affected by this tax quirk up until this point.

It is very likely that from April 2027, MPs will start to experience the same 60 per cent marginal rate faced by many professionals, and that may focus attention on the structure of the system.

Are the income tax thresholds likely to change?

No Government has shown much appetite to fix this. Anaemic economic growth over the past 18-years has left successive Governments searching for ways to make the books balance as spending needs continue to climb. This peculiarity of the tax system raises tax revenue quietly and affects a relatively small group of people. A cynic may wonder whether that calculation will shift if MPs themselves fall into the bracket.

Possible options for change include:

- Increasing the £100,000 threshold

- Removing the Personal Allowance taper

- Redesigning the higher-rate bands entirely

None of these would be simple, and each has a cost to the Treasury. If I could wave that particular magic wand, I’d remove the taper entirely.

Tax tips for income over 100k – What can you do?

If your income sits near £100,000 the key concept is “adjusted net income”. That is the number used to decide whether your Personal Allowance starts to disappear and reducing it can restore the allowance and avoid the 60 per cent band.

Common approaches include:

- increasing pension contributions

- using salary sacrifice where available

- making Gift Aid donations

- managing when and how bonuses are received

These are not complicated strategies. They simply require awareness before income crosses the threshold.