The Lifetime Allowance was the total amount you could build up in your pension during your lifetime without incurring a tax charge. This limit has now been removed, replaced by two new allowances. These will affect both Defined Contribution and Defined Benefit schemes even though these are managed very differently.

What is the lifetime allowance?

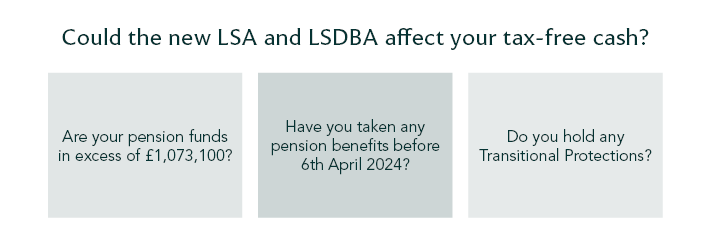

The Lifetime Allowance limited the amount of pension benefits you could build over your lifetime without a tax charge. While the abolition was announced in March 2023, it did not come fully into effect until 6th April 2024.

There may be future amendments to these rules and pension legislation is always subject to change. “Pension legislation doesn’t get simpler. It only gets more complex. That’s why planning and investment reviews are important. There’s always a potential to change, but you can only focus on the now, and deal with the current legislation.”